REAL INDICATORS

“Once upon a time there was a ugly duckling…” Everyone knows the happy ending of Hans Christian Andersen's fairy tale, capable of tormenting its characters, and the little readers who identify with it, with stories bordering on cruelty, before relieving them with the final release. Someone will also remember an advertising version in the legendary Carosello, with Calimero the black chick that it was just dirty (after all, a commercial cannot last as long as a feather moult, but a wash can!).

La amazing recovery post-pandemicItalian economy it has something of a fairytale, but not a miraculous one, being the daughter of harsh transformations and of active repentance in European macroeconomic policies. Let's tell it and frame it in the current global context.

The background, or the period of ugliness and filth. From the beginning of the new millennium to the last pre-Covid year la economic growth of Italy it was wholly unsatisfactory. We have left by the wayside more than one point of lower GDP growth per year, compared to the other major condominiums of the single currency. Cumulative it is over 20%: for a family it would be like stopping earning and spending in mid-October and starting again in January, compared to a German or French one. Other than belt tightening! And to think that the Germans point Italians like cicadas which distribute generous pensions (another fake if we consider unitary annuities!).

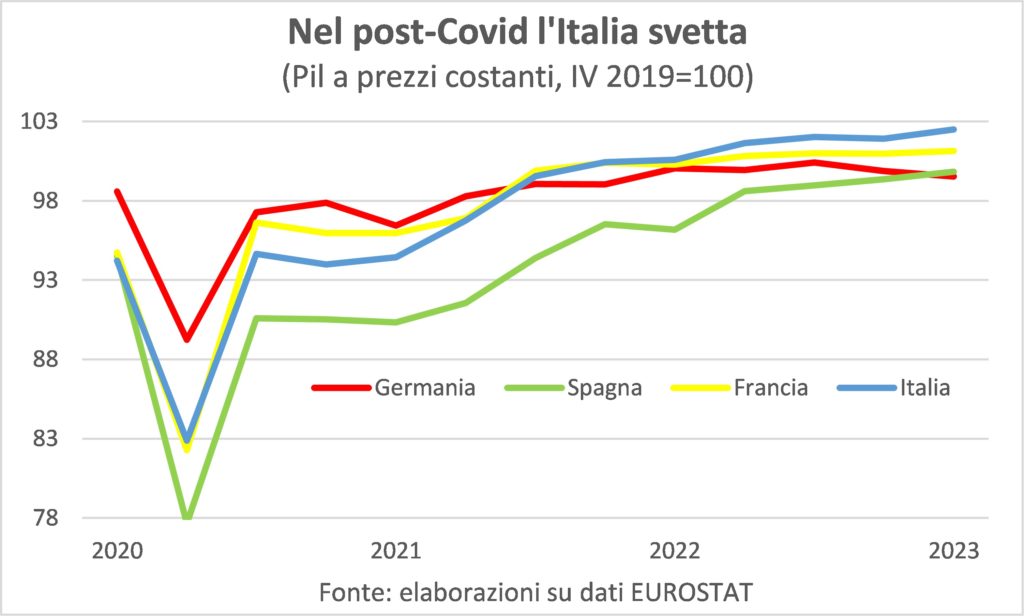

Then, since the start of the recovery from the COVID crisis the the Italian step has become quicker and in the first quarter of 2023 the increase in its GDP is clearly higher than that of Germany, France and Spain.

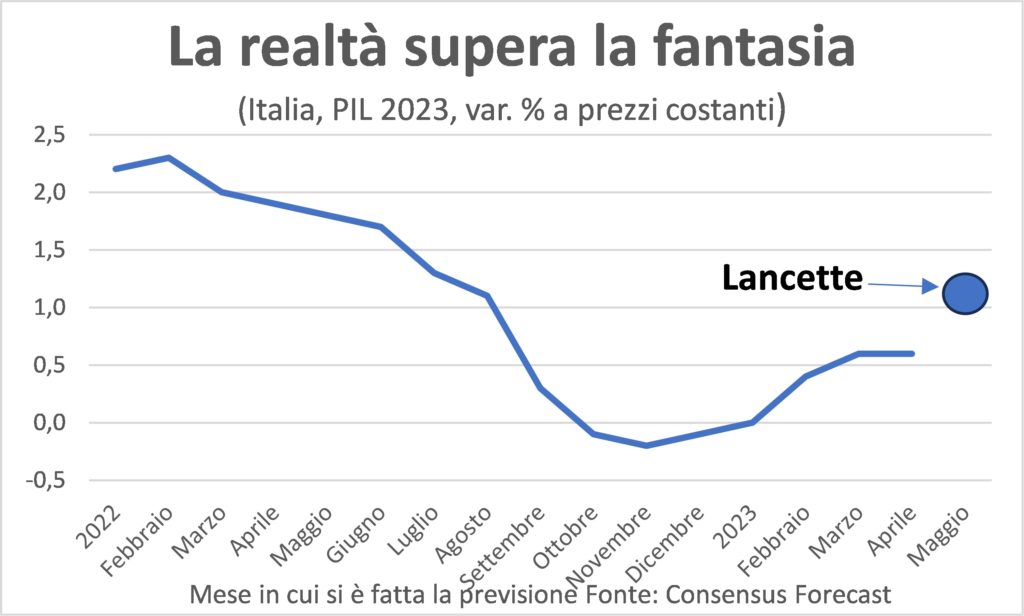

Surprising it is too difference between forecasts throughout the course of 2022 formulated for the increase in GDP in 2023 and the result already achieved: the first, at a certain point last year, indicated a real reduction for this year, albeit small. Now the acquired result is +0,9% and it is very probable that the final one will be a few tenths of a percentage point higher. For heaven's sake: the "Lancette" themselves had bandaged their heads announcing the impending recession, as a result of the war, the double shock, energy and food, and the increase in the cost of money. But more than the tightened belt, albeit slightly loosened by government policies, other factors could have done it. And the observation that reality surpasses the forecasts serves precisely to go and look for the reasons and to understand if they are solid or fatuous.

If we dissect, with the scalpel of statistics, the demand components which have gone from strength to strength these are exports and investments. The former also includes the , and whoever travels the length and breadth of the boot finds armies of visitors filling trains, restaurants, streets and squares, as if it were the last chance to travel in life. But in the former there is also the competitive ability of the business system, aided by a trend of cost of labor much lower than those of European competitors. Companies that are riding the innovations with investments, second galloping component. Also helped by construction in homes (bless the infamous bonuses!) and in public works.

Unit cost competitiveness and new systems (even a bar that adds tables outside the venue creates greater production capacity) have generated a record occupation, which fills the coffers of families impoverished by price increases, which thus can increase consumption, in a dance of supply and demand which resembles that of the planets chasing the Sun moving around the center of the Milky Way (at an unthinkable speed).

ITALIAN ECONOMY: WILL ITALIAN GROWTH LAST?

This dance will last, or as in the game of musical chairs at some point we will have to stop and someone will be eliminated? The experience of recent years has taught us the cardinal virtue of prudence, because ugly ducklings become swans, but if they are black there is no detergent capable of whitening them. But let's look at what will remain and what will disappear, knowing that fairy tales and advertisements are distinguished from reality above all by the lived which remains in the second. Definitely, having conquered market shares in goods and having attracted tourists will continue to make us grow, if customers' trust and experience has been satisfied, and we have no reason to doubt it. As well as the labor cost advantage, on which it would be good to open a reflection on the attractiveness of these wages for young people, many of whom leave; but it does not compete with the Lancette. While we have already written that the redrawing of global value chains favors Made in Italy.

Instead, on the expansion of investment in construction it is legitimate to ask the question: the PNRR And will the other funds allocated by the Draghi government be used to keep actual growth high and therefore raise potential growth? It is a'historic occasion, of those that occur every two generations. Whoever knows how to grasp it will be able to boast of it for some legislatures to come. Anyone who can't do it will see the beautiful swan turn back in Ugly Duckling; or the carriage and the horses in pumpkin and mice, according to another fairy tale whose origins are less Nordic and therefore must be taken very seriously. The "Lancette" cheer for the full and good use of those resources, because they believe in the intelligence of those who lead the country.

And also the markets: the spread between BTp and Bund – litmus test of 'Italy risk' – remains in calm areas, as well as the other 'map': the spread between BTp and Bonos. Especially since there is another structural reason: the improved health of the banking system (copyright Ignazio Visco). On the other hand, budgetary policy effectively supported households and businesses in the dark times of the pandemic, with improvements in their respective finances and the creation of reserves ('private treasures') which made it possible to continue spending, in consumption and investments, as soon as Covid loosened its grip.

For the rest, the international economic framework continues to be in favor of the Italian spacecraft. The data SMEs of Italy are still good, albeit more for services than for manufacturing (as evidenced by the further decline in industrial production in April), but this is a gap that is observed almost everywhere and has reasons we will lean towards next month .

We now observe that we have left behind the catchphrase of the US public debt limit, but that «novi tormenti e novi tormentati mi veggio around» – writes the Poet – and we could write it too, given that on the horizon – both economic and political – stand out other threats. On the one hand, there are growing tensions over Ukraine, where, amid drone attacks on Moscow, more incursions into the Russian city of Belgorod (with deaths), damaged dams and massive flooding, war escalates. Then continue thehigh voltage between America and China, while overlook signs of slowdown of the European economy (with the Eurozone – but not Italy – in a 'technical recession'), but not the Chinese one.

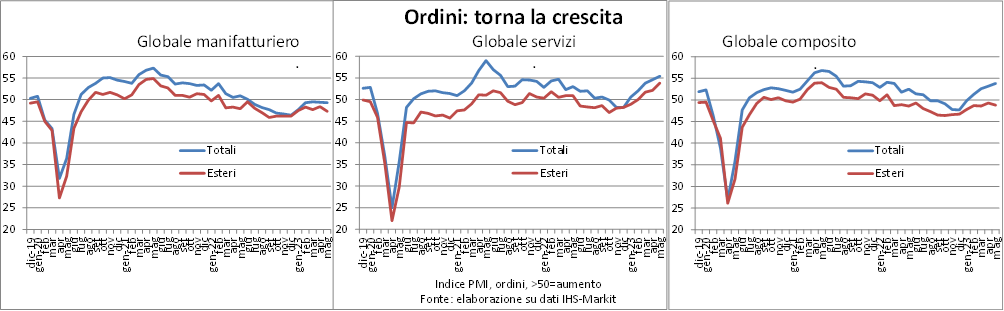

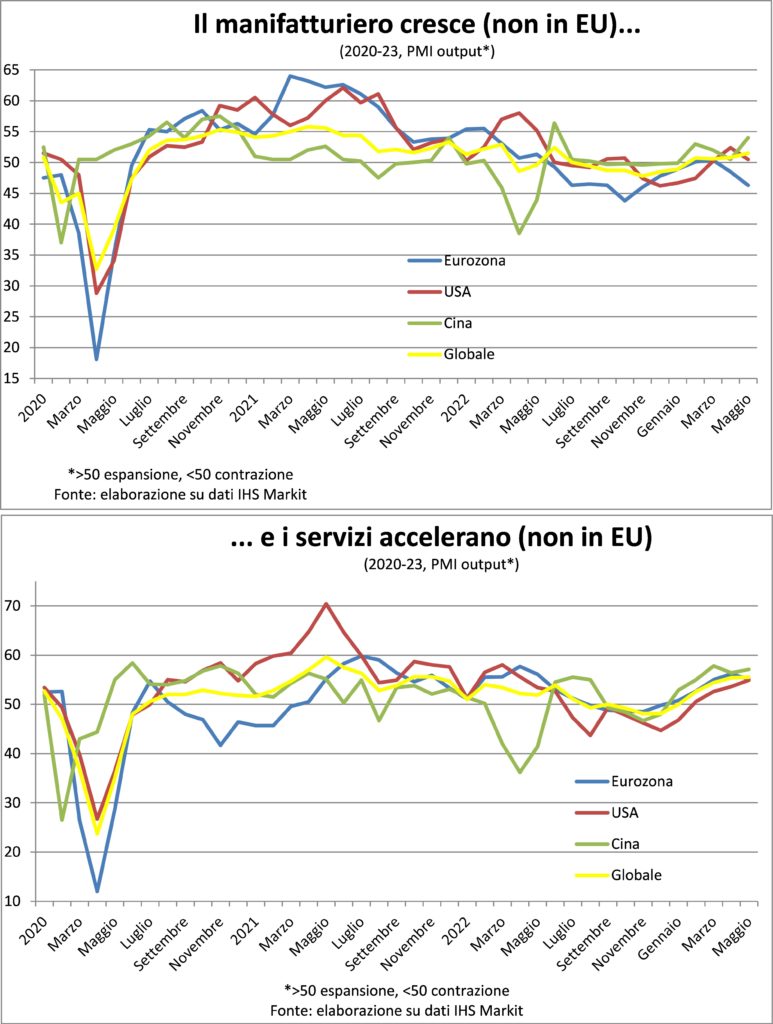

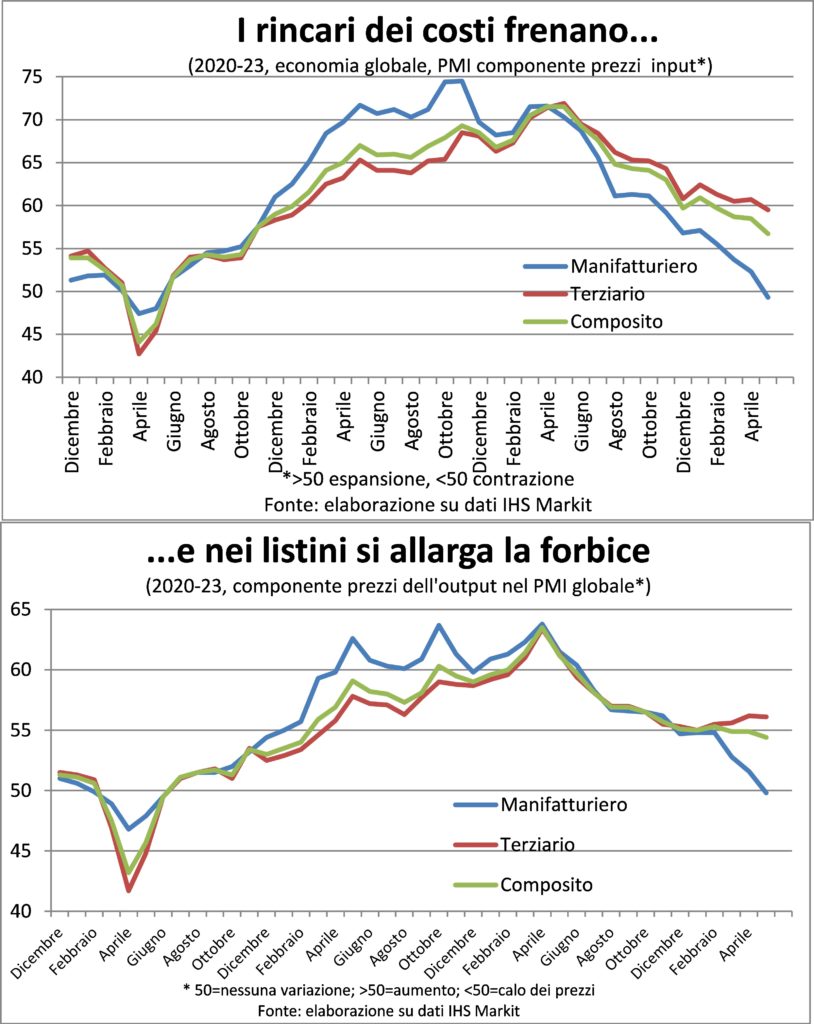

Widening our gaze to the Globe, we observe that orders are growing overall, but as they race in services, they tend to flex in industry.

It's this one industry-service sector gap it is also observed in the present dynamics of production. With an unpleasant addition for us: theEurope appears to be in trouble, either because its manufacturing is contracting or because its services are decelerating, while elsewhere they are accelerating.

INFLATION

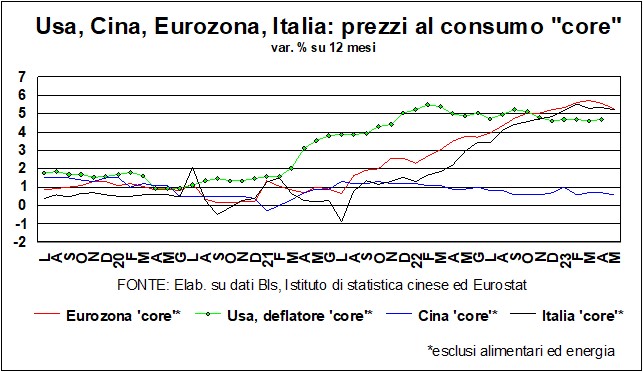

By now everyone agrees that we are in disinflation stage. And we can't help but join the chorus. But with judgment.

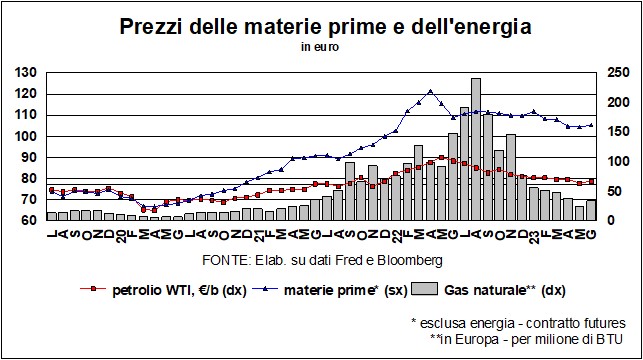

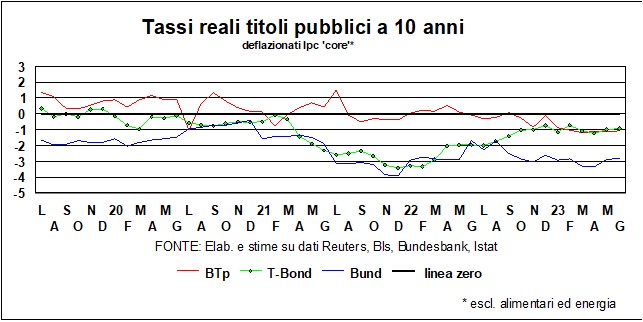

In fact, with i energy prices not too far from the pre-Covid norm (although gas has returned to tearing upwards), while food prices are still high (although also yielding), the temperature of consumer prices is falling.

However, this cooling is not everywhere. Because here too there is a gap that mirrors that just seen in the real economy. The manufacturing firms apply discounts to stimulate demand, aided by détente in the value chains. Those gods services, swollen with requests, pass on the higher labor costs to customers, because wage dynamics are still higher than they were three and a half years ago. And this is clearly seen in the price component of the PMI.

Attention toread properly the data: the discounts practiced by industry are marginal, while the increases in services remain very hot. In other words, it is correct to predict that this inflation will be overcome, but it is not yet the time for central banks to let their guard down.

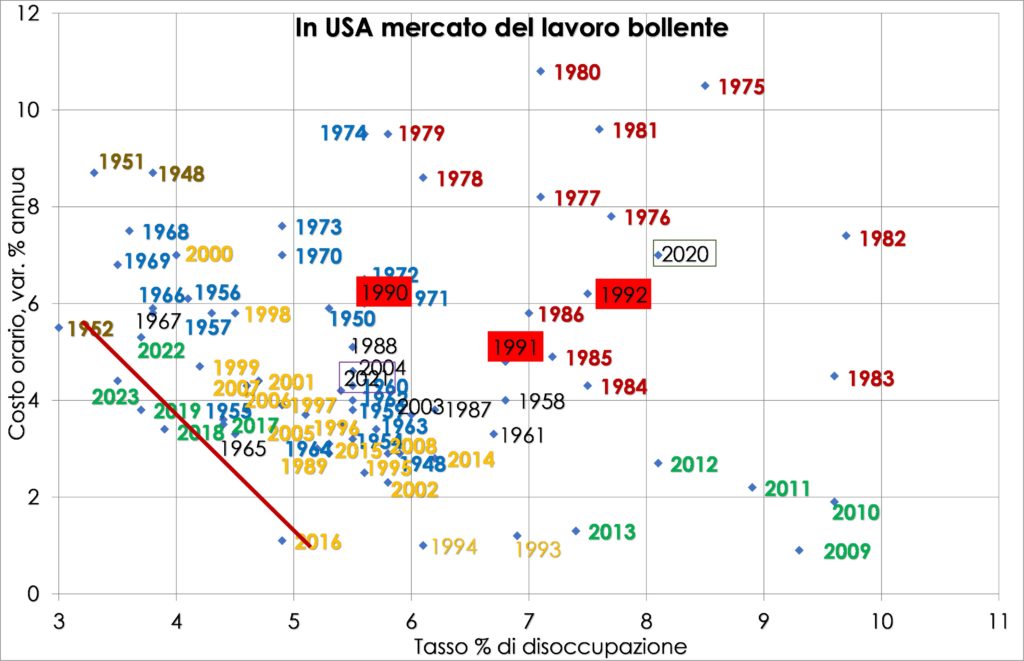

Talking about wage dynamics: one discusses about that USA. Looking at hourly wages month by month, we notice a clear deceleration. Which reverberates on the wage bill and, therefore, on household demand and on price tensions. However, if we remove the effect recomposition of the total number of posts of jobs (from the best paid in the public sector and in manufacturing to the lowest paid in HORECA) then we notice a certain resistance to cooling down, precisely because the American labor market is still hot. For this we invite the judgment in declaring the inflation procedure resolved and archived.

RATES AND CURRENCIES

This time, let's start with stock markets. And let's start with America, since, for better or for worse, it is Wall Street which gives the 'the' to the stock exchanges around the world. Which bags are fine, thank you, but some questions arise. In the thousands of analyzes of the US stock market there is one that tries to calculate the level of the S&P500 net of Faang (Facebook – now Meta –, Apple, Amazon, Netflix, Google – now Alphabet); and the result is that without those the index, since the beginning of the year, would be flat instead of having gained around 12%. And even going further, the Wall Street 'bull' seems to have owed much to the FAANGs and their profits. But maybe the big tech companies are running out of steam. But here comes the AI, theArtificial intelligence. In a jolt that brings to mind the convulsive events of the dot.coms of the late XNUMXs, anything that has a bit of AI inside earns a premium on the Stock Exchange, and this support for prices perhaps explains why the US stock market does not give off signs of a recession (although only a minority of US analysts think the US economy can avoid a hard landing).

But the questions, as mentioned, arise. On the one hand, the data on profits of national accounts for the first quarter, if compared with the quotations of the most comprehensive index (il Wilshire 5000), show that the gap is widening: the former grow much less than the latter. On the other hand, theAI is still young, and seems to have teething problems: the case (reported by the BBC and NYT) of a New York lawyer who defended his client by presenting the judge with a rich analysis of legal 'precedents' in his favor is emblematic. The opposing party's lawyers have found no evidence of these precedents and of the large number of summonses. Finally, it turned out that the lawyer had asked ChatGPT for help, e the AI had made it all up. Perhaps because she was eager to please the questioner (we're sure the technical explanation is different, but we can't think of another). So? Who knows, maybe i 300 million jobs which, say the alarms, will be lost because of the AI will come compensated by 300 million workers intent on checking and sifting through the answers of ChatGPT. And, given that, as anyone who has toyed with the AI knows, it is quick to respond, but checking and sifting are slow, the global total of hours could even increase…

In short, some shadows hang over the Stock Exchanges – even if (readers know the refrain) – in the long run the drawers will win.

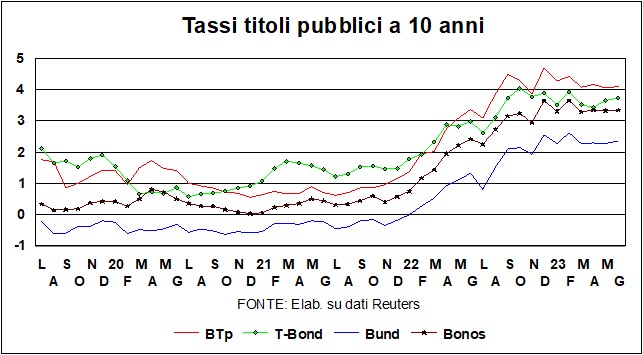

And we come to rates. Pause yes, pause no… Guide rate hikes in Canada and Australia they report that the Central banks they are still worried about inflation: it slows down, but not enough, and wages are still busy recovering the lost purchasing power. Thus, from the 'yes pause' we moved to the 'no pause', and yields, both nominal and real, have risen, with the curves that remain inverted both in the USA and in Germany.

How long will it last the frown of central banks? There are two reasons to think that the 'pause' will return to the horizon of possible and probable things. On the one hand, the economy holds but loses some blows; on the other side, disinflation proceeds, slow but inexorable; and finally, to the extent that the Banks must also take into account the geopolitical risks, these are on the rise.

Then, for the Usa, there are those who think that, following the debt limit agreement, the Treasury will proceed to massive emissions of securities (to replenish the liquidity reserves drained in the agonizing wait for the agreement), and these sales of securities they will deprive the economy of liquidity. And analysts say the Fed could 'pause' because this liquidity drain is 'worth' a quarter point hike in rates. Perhaps, but in the months in which the Treasury used its reserves to spend and scatter, the economy received liquidity, and the fact that today this is being drained by emissions should not change the underlying situation. Before the hemorrhage of funds from the Treasury had lowered rates, now the transfusions of funds from the market bring them back up. But in any case, they will continue the monthly sales of securities in the Fed's belly, and these drains will be able to induce banks to be more selective in loans.

As stated above, i btp they are in relatively quiet territory. 'Relatively' because the rise in yields is always negative for a country with a high debt, but at least there are no Italian demerits in this climb, as demonstrated by the stability of the spread. Indeed, the 'merits' are increasing, there is a positive feedback between higher-than-expected growth, political stability and attractiveness: for example, Blackstone, one of the largest investment managers in the world, has announced that it will favor Italy for direct investments.

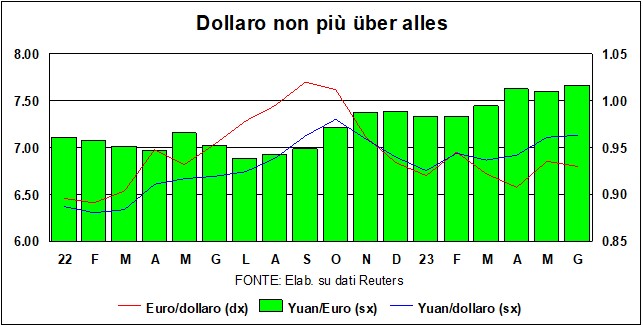

In the foreign exchange markets the dollar has withstood the attacks, mostly verbal, of those who predict the descent of the greenback from the highest podium of world payments: the Russia, the China, Brics expanded plan to remove from the dollar what, in the XNUMXs, Valéry Giscard d'Estaing called a “exorbitant privilege” (and, among other things, depriving the dollar of that prominence in financial systems would facilitate the circumvention of the fines).

This is easier said than done. Ben knows it Russia which, after negotiating with India to be able to settle bilateral exchanges with the respective currencies, now, after having sold a lot of oil to India, it finds itself with a lot of rupees that it doesn't know what to do with (it should recycle them into other currencies, but cannot due to the fines…). However, after hitting 1,10 against the euro, the greenback is stabilizing around 1,07, and there's no big reason to jerk higher or lower. The yuan it settled well above 7 against the dollar, and depreciated by 6% compared to a year ago – and by 9% against the euro. A useful change for a country that is struggling to get back on the path of growth.