REAL INDICATORS

“Maybe it was the right time?!” was the motto and lifestyle of bartender from Ceccano, the character invented by Nino Manfredi in Canzonissima. Almost three generations of Italians ago, black and white TV, only one channel, broadcasts that started in the late afternoon and ended at midnight at the latest, and cathode ray devices purchased in working-class neighborhoods with collections. Nothing to regret except theoptimism expressed in the joke with which the sketch ended: continue to smile and laugh, always hoping that it will be the right time. And if 2024 was really forworld economy and the Italian one, with a trend without surprises and troubles?

Against all prejudices and all superstitions, theleap year it could be less disastrous than the three years that preceded it (if only because February 29th, an extra day, adds 0,3% to GDP...). On a purely economic level there would be all the premises, although in the last three years we have learned that the real surprises, at least the negative ones, come from other theaters of human deeds. So, in the spirit of the bartender-Manfredi, let's browse through daisy of economic fortune, starting with news on real variables.

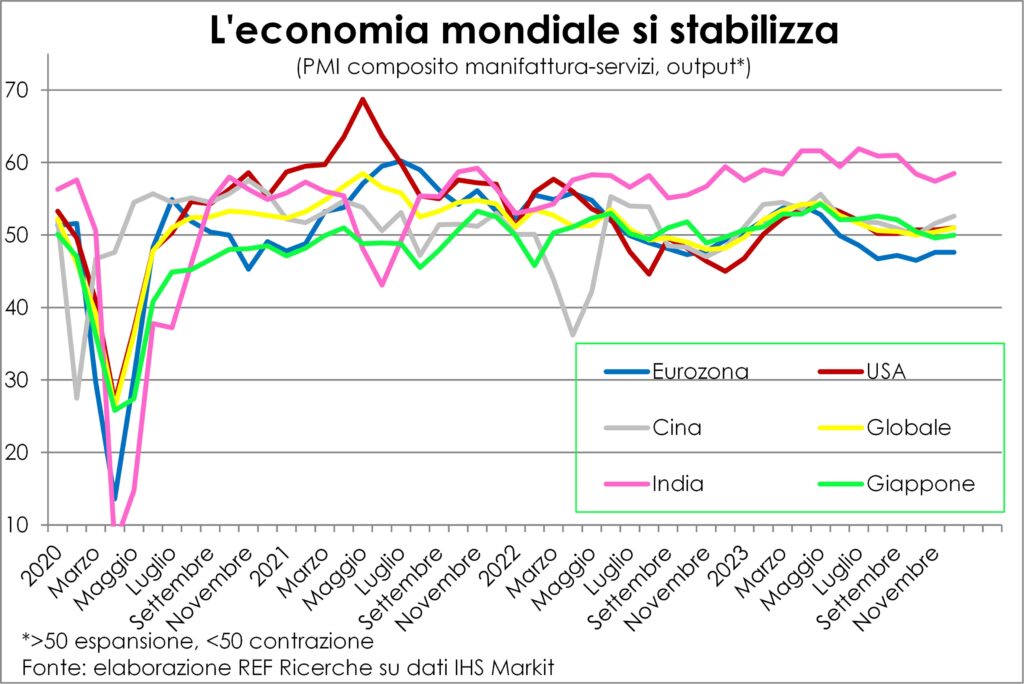

La overall production at a global level it is stabilising, despite the strong geographical and sectoral differences that we observed in the second half of 2023. We see this in the output component of the composite manufacturing+services PMI.

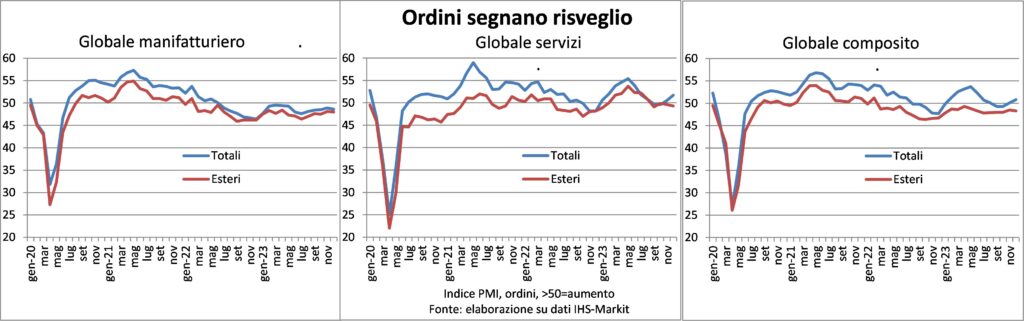

Le geographical differences are clear: Asia, pulled by China and India and ballasted by Japan, it's better than USA, which fare better thanEurozone. The latter is penalized by some contingent factors and others less. Among the former, manufacturing, which weighs more here than in America, is affected by the fact that demand has turned to the tertiary sector to satisfy the social desire and that consumer and investment goods are more cyclical and sensitive to financial conditions; the difficulties of German federal budget, after the ruling of the Constitutional Court on the green reuse of some funds voted by the Bundestag for the pandemic (60 billion are not even small amounts for Germany), and the countermeasures are proving to be very painful and are triggering unusual street protests for the people Teutonic. Among the less contingent factors, the transition to electric motorization it significantly reduces added value and employment in the main industry sector, the automotive sector, not only in France and Germany, but also further east (such as in "European Detroit", Slovakia). Even for future production, which ones they are the orders, there are signs of awakening from the stagnation into which the global economy ended in the second half of 2023.

In this case too, that's all merit of services, because manufacturing orders continue to contract, albeit at a slower pace than last June-July. The level of stocks is falling and entrepreneurs anecdotally note that they have little visibility for the months to come, but many of them believe that the worst is underway and that the second half of the year will be better. Between nations, the report card of the good (where demand increases or decreases less) and the bad (where orders fall more) sees very few happy islands in manufacturing (Austria, Philippines, Indonesia, South Korea, China, Italy, India), which instead are the vast majority in services, both in number and weight, with the sole exceptions of Australia, France and Germany.

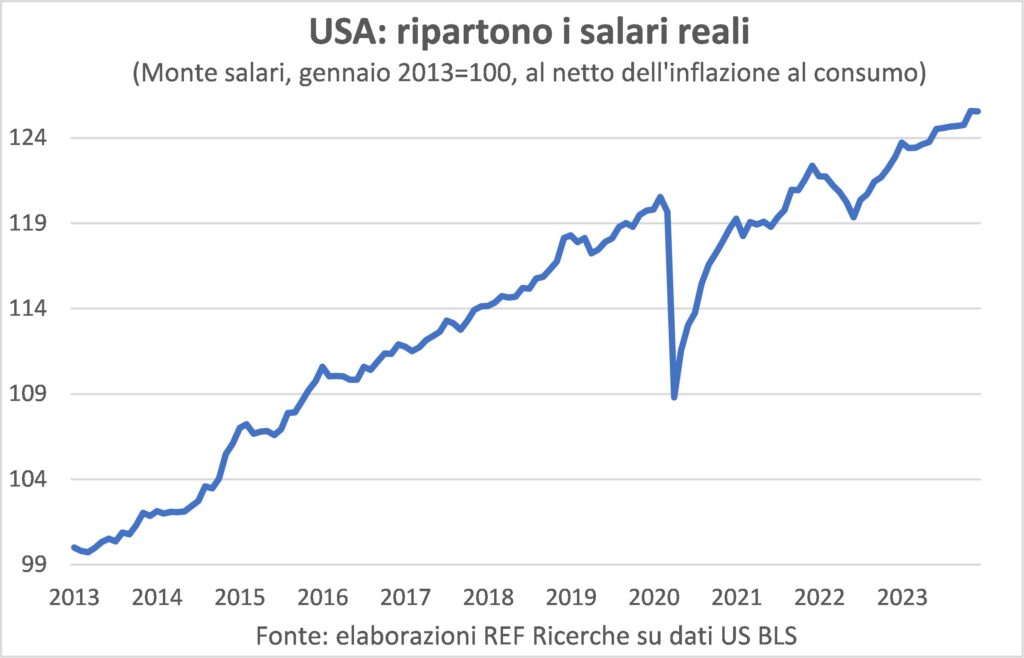

Le better notes in the general picture (we leave the painful ones at the bottom) they come from job market at every latitude. Three statistics deserve to be highlighted: theexpansion of employment in the USA, that in Italy and the further decline in unemployment rate in the Eurozone. For the first two, i American and Italian jobs are advancing at the same pace for many months now, and progress in both markets is giving confidence and purchasing power for families. A similar improvement in confidence and income is observed in the Euroarea. Here we use US data on real wage bill as an example of common conditions.

In fact, the job market is everywhere in the hands of the seller, given the wide gap between vacancies and unemployed people. This generates a upward pressure on wages. Until a few months ago, companies had managed to defend unit margins and increase total ones, but in manufacturing this defense has given way to the fight for market shares, while in services higher costs continue to be passed on to customers. This brings into question the issue of inflation, which we talk about below, immediately anticipating that the good news prevails. Another reason for optimism and consumption support.

If the poison is in the tail, here's the less reassuring news. Apparently they are a common ailment that does not generate any joy. The main risks are political, whether manifested in the electoral results or in the Munchian scream caused by the use of weapons. This year they go to the polls several billions of citizens, from India to the United States of America, from the European Union to Bangladesh, from Russia to Indonesia, from Pakistan to Taiwan. The votes from which they can arise destabilizing consequences they are certainly those of US and Taiwanese citizens: in the first case due to the internal split within society, in the second case due to the reaction they could induce in the gigantic neighbor, who feels like the master of the house (how can we forget the fairy tale of the wolf and the 'lamb?).

On the surface, these risks appear burden equally over the entire world and have the same reach. At a closer look, they are there large asymmetries. For example, it is difficult to say whether and to what extent one outcome or another of the US presidential elections could affect the fate of the world's largest economy (at current exchange rates) and therefore the rest of the global system. Conversely, if there was one bloody invasion of Taiwan direct and indirect damages would be very high; there are those who indicate them at 10% of global GDP, even if the quantification should be taken with a grain of salt. Furthermore, while the United States is far from the wars waged and little directly influenced by what happens in the Red Sea, Europe is damn close and more exposed to the consequences of the blockade of that important maritime communication artery.

To recap, 2024 growth will be low compared to what was observed in 2021-2023, because the pressure on the monetary brake exerted by the Central Banks continues to impact, especially on industry (including construction), although the system is withstanding the tightening much better than feared (thanks to the absence of financial imbalances), and why the post-pandemic rebound is over. But there will be no global recession and inflation will continue to fall. In short, a soup that is neither too cold nor too hot, as people like it Golden curls.

INFLATION

About the price dynamics, there is a downward convergence. It is not a divine gift nor a fortuitous astral conjunction, but the result of the operation of market forces and prudent policies.

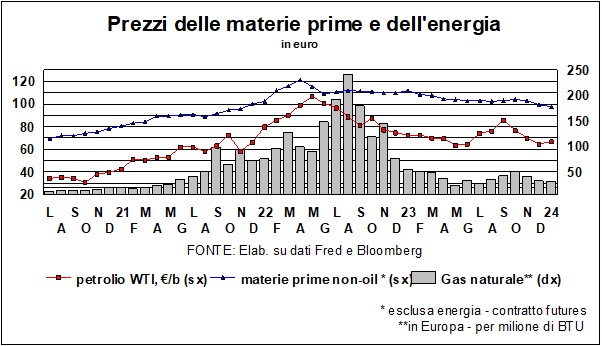

Let's start with the king of raw materials, the Petroleum. His prices have been declining since the end of the summer, and only the unfortunate developments of the Middle Eastern war have made them ripple. This, together with the price trend of the gas (-46% over twelve months) and dei foodstuffs (-10% the FAO index during 2023) explains a lot about the speed of the decline in total consumer prices.

Two questions: what is the origin of it and what will happen now?

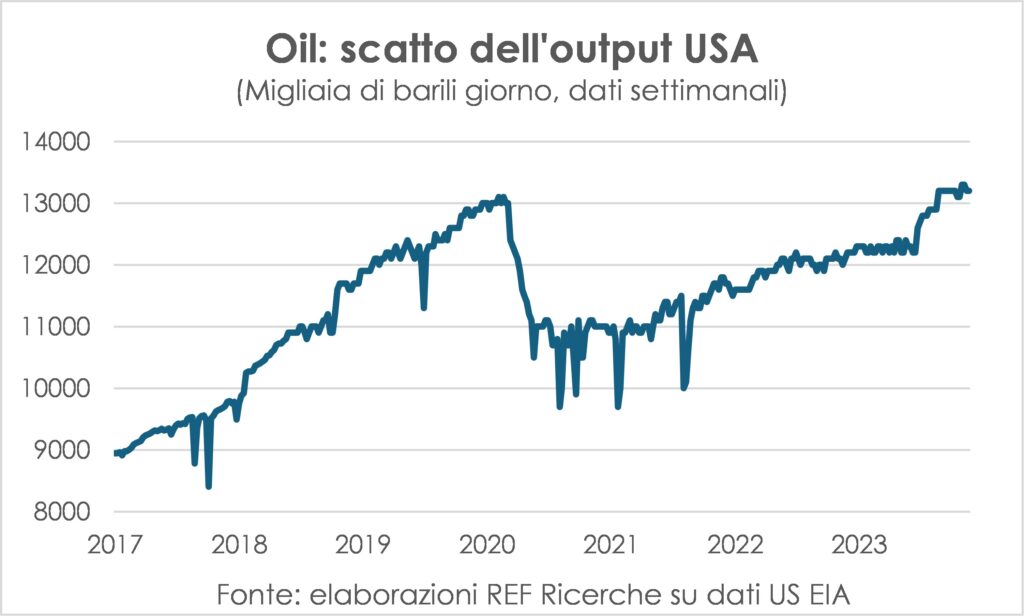

Le Lancet of December argued that they were behind the decline in oil and gas prices supply and demand reasons: weak demand and strong supply, the latter for Russian extraction, indifferent to sanctions because it finds customers outside the West which is no longer the center of gravity for the fate of the world. Within the bad news of the ineffectiveness of the sanctioning weapon there is the consolation that theworld economy is less weak than feared. A further investigation strengthens this deduction: the USA production it recorded a spurt right from the end of August and reached new historic highs.

Now it is unlikely that US supply will rise much further, given that it has reached the ceiling reached before the pandemic; however, we have learned that at these prices it shale oil is very profitable and therefore new wells are opened (the current pace of new drillings is tall, but not very tall). On the other hand, the gradual restart of the economy is likely to fuel greater demand. So we can keep these prices as stable, barring any surprises.

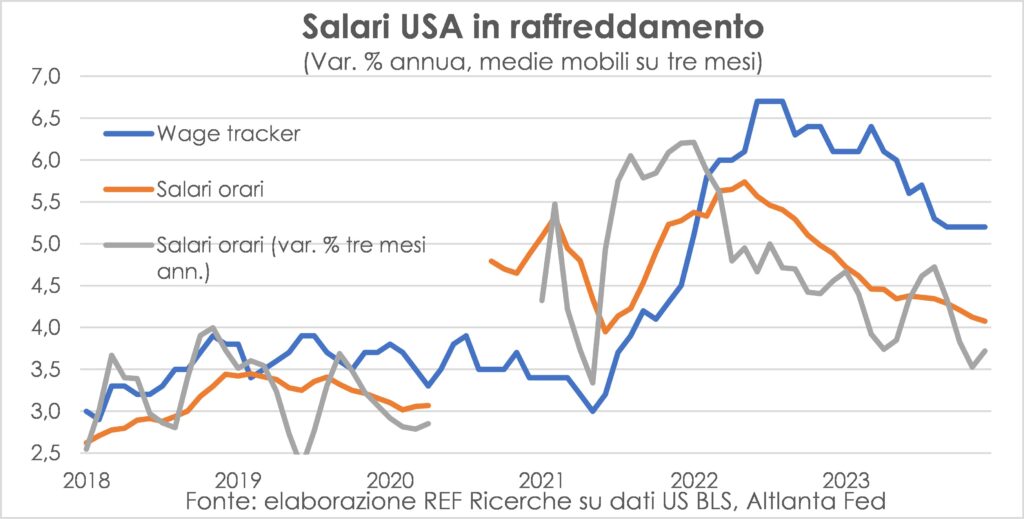

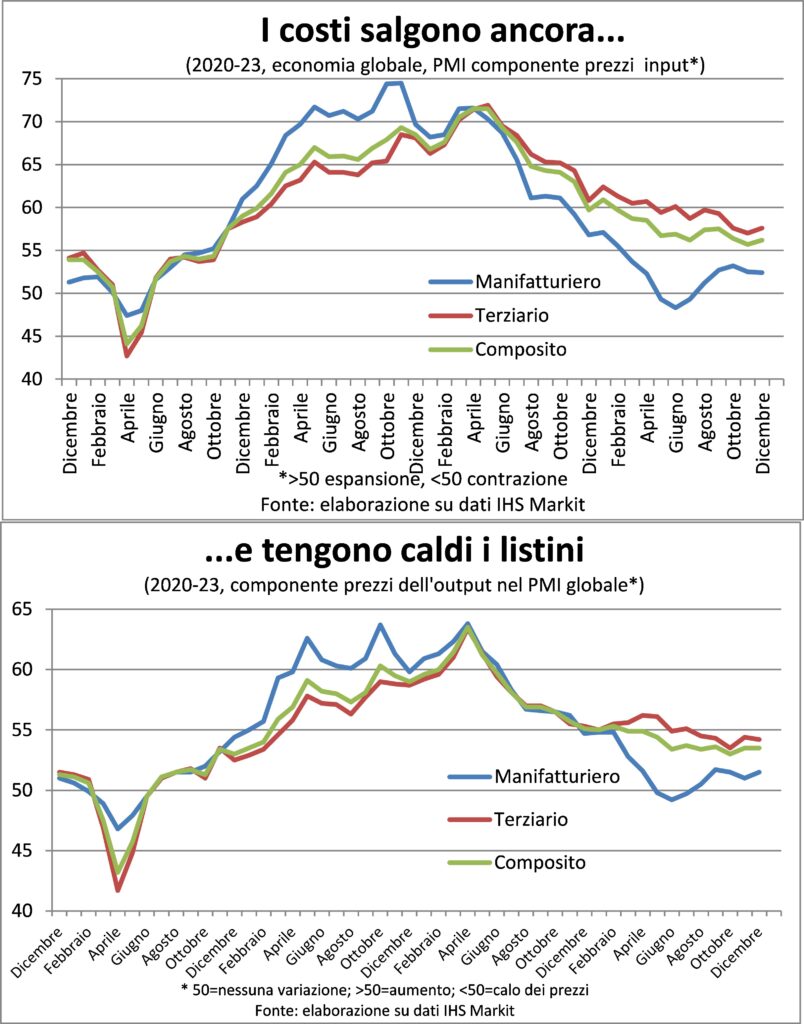

It is interesting to extend the question of is what will happen to all the factors that make up the inflationary framework. The answer, already advanced in the past, is that the quick and easy part of disinflation is behind us, and that now the drop in temperature of consumer prices will be more gradual and will take time. Why the king of costs, that of work, continues to increase thanks to the worker shortage conditions already illustrated above and to regain some of the purchasing power lost in the last two years. In the United States the wage dynamics it is moderating, but it will not return to the values of 2019, when it was believed that the greatest danger was still deflation.

Indeed, in PMI surveys, businesses continue to report wage increases as the largest source of price increases, which at a global level continue to increase more than in the period before the pandemic, although the gap has closed significantly.

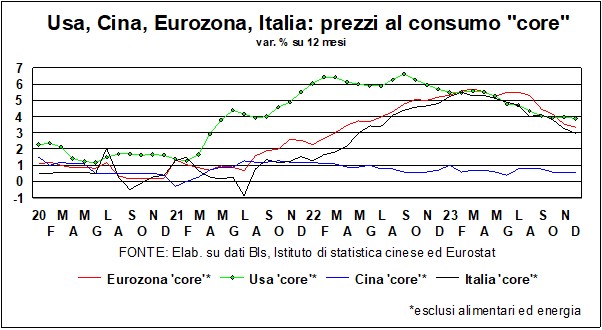

On the other hand, both in the USA and in the Eurozone the cooling of final demand has already borne considerable fruit. And the current trend of consumer prices of both the total dynamics and that net of energy and food moves towards a stable return to 2% or a little more towards mid-2024 in the USA, while in the Eurozone this has already happened in December. Another good news for Ceccano's bartender, and for all of us.

RATES AND CURRENCIES

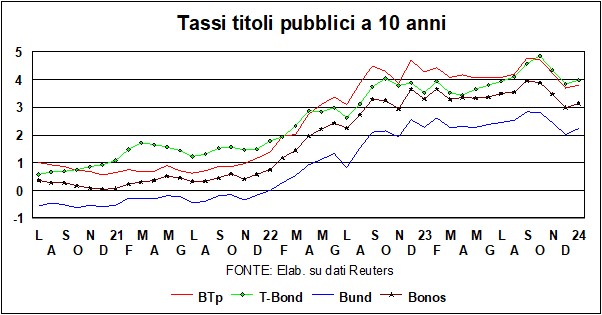

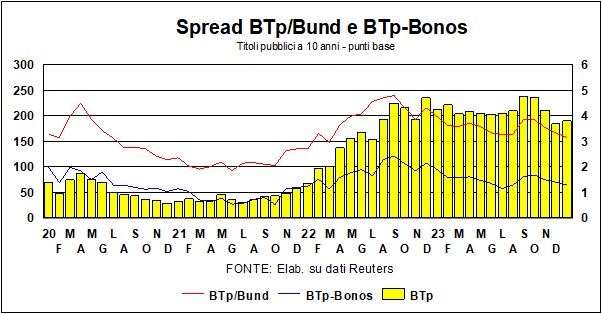

Il modest retracement of rates on government bonds is probably due to some previous excess of optimism, but the underlying trend remains: i rates have come down from the highs, and they want to go down further. A 'desire', this, which belongs more to the markets than to the Central banks, who aim to see the decline in inflation in the white of their eyes before starting to lower the key rates. Which guide rates are still restrictive: higher than the inflation rate, both in America and Europe, and compared to the index headline that to that core of consumer prices.

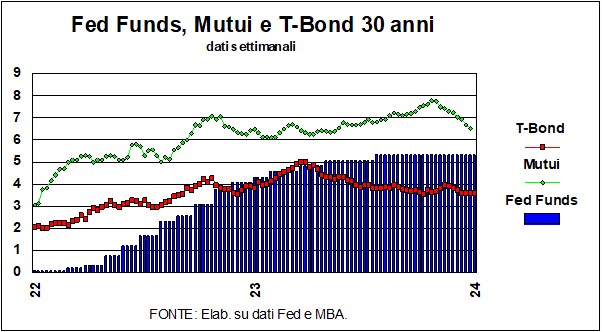

The discrepancy between the Fed's severe stance and the good-natured attitude of markets can be seen in the graph, which compares the Federal Funds policy rate with the trends of the 30-year T-Bond and 30-year mortgages. The guide rate has remained unchanged for months, but i mortgages – which have antennas that are very sensitive to interest rate expectations – they saw a rapid decline. The same thing can be said for long yields bond municipal bonds (which yield much less than T-Bonds because they are tax-free – not even our 12,5%!). And another indication of expectations of decline of rates can be found – both in America and in Europe – in the purchase of public securities: the latest issues of long securities were enthusiastically subscribed for multiples of the quantities offered – from Belgium to Spain, to the United Kingdom, to Italy…. In America, this week the 3-year T-Bond - a maturity that is most affected by the probability of falling yields - was sold at the lowest level since last May. In short, investors they want to ensure still high returns, before the decline. The phases of declining rates are favorable to Italy, as can be seen from the spread, which has dropped at the lowest level since the beginning of the Meloni Government, both towards the Bund and Bonos.

Investors will be disappointed? Doubts arise from both supply and monetary policy factors. As for the supply, in America and elsewhere the next few months will see massive financing needs from governments (who also put some hay in the farm with the latest issues). Regarding monetary policy, The Fed and the ECB may be slow to lower rates. Concerns about inflation have moved from prices to costs, in the sense of the cost of labor, which is the primary input for the formation of prices. As mentioned above, the dynamics of labor costs is on the rise, both on this side and on the other side of the Atlantic. However, by throwing in a bit of productivity, and taking into account the ongoing disinflation of goods prices, the inflation dynamic could remain within the range desired by the Central banks (who are cautious by profession). In short, the markets have a good chance of not being disappointed.

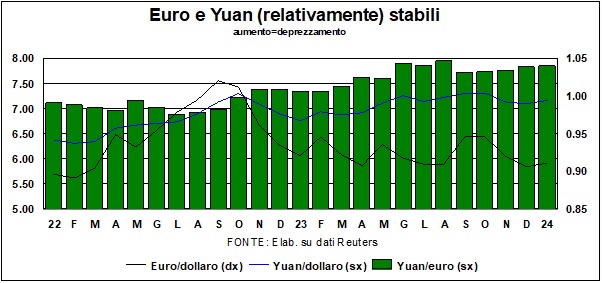

On the foreign exchange markets, the dollar continues to remain within the range mentioned last month (1.05-1.10 against the euro), with some attempts to tear upwards (i.e., to depreciate). But it's interesting to look at – see graph – ai effective dollar rates (against 63 currencies), nominal and real. The graph shows that, from the beginning of the pandemic to today, the dollar has not changed much against the euro, but has appreciated compared to all currencies, and even more so as a real exchange rate (based on consumer price indices) . This appreciation owes a lot to both muscles of the American economy than to good (comparative) performance as regards inflation.

The Chinese currency has not changed much, and confirms that China needs one yuan competitive.

E the stock markets? The stock markets have done a lot in the past year better than expected. Here too, could the supporters of equity investment (among which we are, as we repeat at every 'Lancette') be disappointed? Let's take things at a distance. The 'Holy Chalice' of investment fund managers is a formula that describes the ideal composition of a small activity garden, such as to bring both the benefits of 'tranquility' (relative, of course) of bonds than the adventurous ascents (and descents) of the actions. How much - the managers must decide - to put in shares (domestic, international...), how much in bonds and how much in safe haven assets (starting fromgold, which also suffers from congenital sterility, in the sense that it yields neither dividends nor interest, and, since Russia's invasion of Ukraine, has increased no more than the S&P500, which instead yields dividends).

The last few years, filled with black swans, have been particularly difficult for those seeking the Sacred Chalice. The famous 60/40, the best known of the recommended proportions for a prudent and profitable portfolio, recommends 60% in stocks and 40% in bonds. But does this 60/40 stand up to the tests of financial history? An interesting recent essay published a few months ago by the National Bureau of Economic Research (“Beyond the Status Quo: A Critical Assessment of Lifecycle Investment Advice”, by Aizhan Anarkulova, Scott Cederburg and Michael S. O’Doherty) reaches a revolutionary conclusion: 60/40 should be changed to 100/0, i.e. all in stocks (half domestic, half international). Of course, a lot depends on the investor's horizons. If today you have collected the proceeds from the sale of the old house, and in a month you have to pay that money to move into the new house (a roof is needed...), it is not advisable to invest the nest egg in shares: it is better to stay calm and keep them in the bank. But, for the medium-long horizons - those typical of the drawer - the economists mentioned above have no doubts (of course, it will never happen, because the bond market cannot dry up…).

The analysis was conducted assuming many mixes of shares and bonds, differentiated by geographical areas of the stock markets, by issuer (public, private) and by age classes of investors (for example, another common recommendation is that young people should hold more stocks than bonds). And reaches the above conclusion, valid for every country and for every age group. The authors recognize that, in periods when stock markets fall (price volatility is much higher than bond prices), there is a strong temptation for the investor to throw in the towel and sell at least a portion of an investment which, it is feared, could continue to lose value. Faced with this temptation, the authors recommend stay still and wait for good weather. This is a recommendation that should also apply in politics, where many necessary reforms unfold their effects over longer periods than electoral cycles...