The new provisions on automatic enrolment in supplementary pension schemes for workers have come into force on 1 July 2026. private sector employees.

The new rules concern the destination of the TFR accruing at the time of hiring and distinguish between first-time workers and workers who have already had previous employment relationships.

TFR: New rules for first-time workers

I first-time workers, have at their disposal 60 days to refuse with written form the automatic conferment of the TFR to the collective pension scheme applied in the company. A clarification is already necessary at this point: what does the first hiring refer to? It certainly refers to the first entry into the labor market with the related employment relationship. It would therefore seem that the new regulation applies to newly employed. But what happens to a worker who is hired by another company and who has perhaps already joined a supplementary pension scheme? After all, for this individual too, it is a first-time hire at the other company with which he or she is establishing a relationship for the first time regarding the accreditation of a new severance pay. The employer is always required to practice the silence/assent formula Unless a refusal is expressed within the required 60 days, during which time the employee can indicate to the employer which fund to allocate the accrued severance pay (TFR). The employee cannot opt to retain the severance pay in the new company unless the employee has fully redeemed their position in the previous fund.

Taking into account the ordinary mobility within the labour market, this mechanism could determine a process of implementation of memberships Through the form of silence/consent superior to that referring to the occupation of the first job. This would seem to be the correct position, but it deserves clarification.

Essentially, the very dynamics of the labor market (especially with permanent contracts) are driving the adoption of supplementary pension plans toward a trend toward negotiated and collective pensions. What scenario—after thirty years of experience—is this "turning point" (already anticipated in collective bargaining agreements in some sectors) affecting this? The Covid Authority, the sector's supervisory authority, has been tasked for years with monitoring the investments of the self-employed workers' funds, and has provided an answer to this question through its comprehensive annual reports.

The supplementary pension system in Italy

By the end of 2025, the system had 273 supplementary pension plans for overall 10,425 million members, 4,8 percent more than in 2024. In relation to the labor force – the aggregate including employed people and job seekers aged over 15 – the participation rate rose to 39,9 percent (38,3 percent in 2024); if referred only to individuals who paid contributions in 2025, it stands at 29 percent (27,6 in 2024). That is, there are approximately 2,7 million members of tax evaders who do not increase their contribution amount at the expense of the amount of their future private pension. The possibilities of advances (for purposes other than social security) and redemptions. These options are real "bribes" that the capitalized pension pays to the TFR which is its main source of financing and which forces, for simple reasons of convenience, the amount intended for the supplementary pension to provide the same opportunities ensured by this pay institution (precisely the advances and redemptions for very high portions of the accrued amount through the payments of severance pay and contributions from the social partners).

Here it is the great misunderstanding of Italian-style supplementary pension provision This has ended up being—due to its dependence on severance pay and its rules—a capital investment, favored by its tax treatment (€5.300 in deductible payments per year), by the severance pay's current availability (not at the end of the employment relationship), and by the contribution that the employer is usually required to pay based on the contractual obligations it establishes.

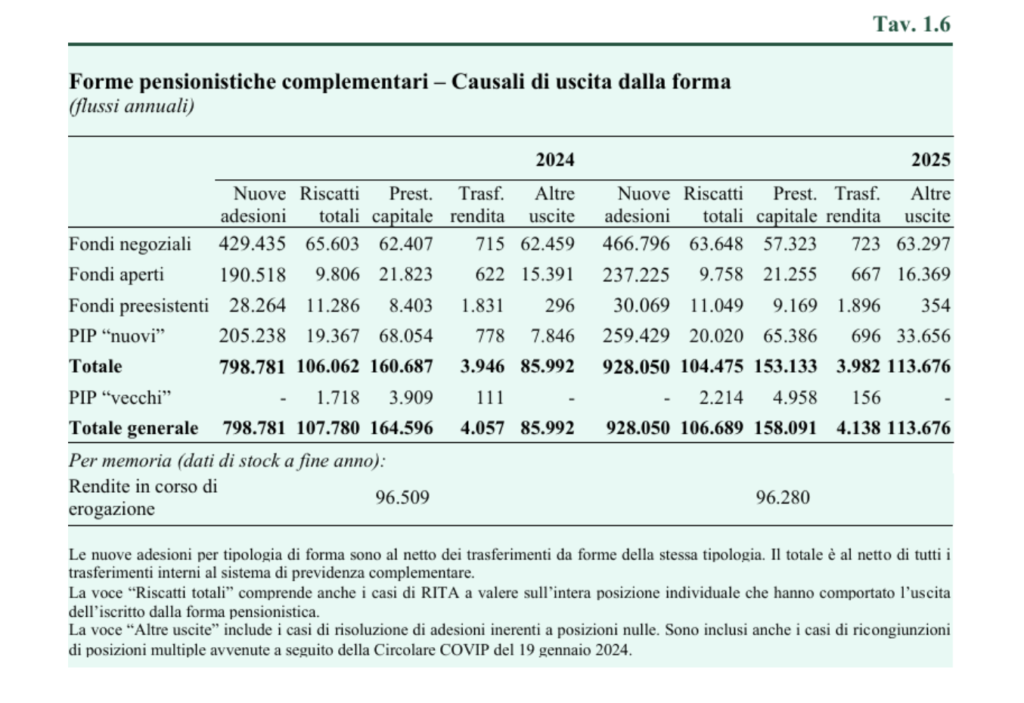

For exits from the pension scheme (i.e., the provision of the benefit), total redemptions remained stable in 2025 at 106.700, three-fifths of which were in the negotiated funds. This item also includes the exits from the system resulting from RITA, applied to the entire individual position and fully paid: 5.300 units in 2025, of which 3.900 in pre-existing funds. These sums represented a trip to the rescue of compulsory retirement and a decline in private pension provision. New pension benefits involved 162.200 positions, down 6.500 from 2024; the majority consisted of lump-sum payments. Positions converted into annuities remained stable at 4.100, thus remaining modest. Total annuities being paid at the end of 2025 remained essentially unchanged: 96.300, almost all of which related to pre-existing funds.

The fact is that the transformation of supplementary pension provision into a financial operation (capital liquidation up to 60%) compared to the guarantee of a second pension is further encouraged precisely by the reform entered into force on July 1st, thanks to those who are called "flexibility of collection". In fact, they have been introduced three new options which still make liquidation in capital is more convenienta) The first involves the payment of a fixed-term annuity, equal to the member's expected remaining life. During this period, an annual payment is equal to the ratio between the accumulated amount and the number of remaining years. The consequence of this choice is that, if a member lives longer than expected, they will no longer receive any benefits. b) The second option allows the member to decide not to collect one or more annual payments and subsequently make withdrawals up to the total amount of uncollected payments. c) The third option allows the member to collect the accumulated amount in installments over a period of no less than five years. The Pension Fund Supervisory Commission will establish the minimum number of installments and their frequency. This benefit is taxed similarly but differently than annuities, as a 20 percent withholding tax is applied to the taxable portion, which is reduced by 0,25 percentage points for each year of participation in supplementary pension plans exceeding one fifteenth, up to a minimum of 15 percent.

Since new registrations combined with new hires since July 1st are crucial, it is important to evaluate their flows over an appropriate time frame.

Annual flows of new registrations Indeed, they provide insights into ongoing trends in the diffusion of supplementary pension provision. New enrollments in 2025 totaled 757, 105 more than the previous year. Among individual forms, the largest share was represented by collective pension funds, with 356 members; contractual membership, equal to 43,2 percent of the total, is significantly lower than the previous year, when it accounted for over half. The remaining flow of new enrollments was split between PIPs, with 209 new members, and open-ended funds, with 179 members; existing funds accounted for a significantly smaller share. The data relating to PIP and open-ended fund membership, which are growing, compared with those declining through contractual arrangements, demonstrate that there is a demand for private pension provision that is not matched by the offerings of the collective entities entrusted with the constituent role of the sector.