Europe has awakened

It's really waking up Sleeping Beauty in the Woods? The beauty is theeconomy of the eurozone and the forest is much thicker, darker, and full of dangers than the one in the fairy tale of the same name. Between geopolitical tensions, the arms race, the reshaping of globalization through tariffs and counter-tariffs, the AI revolution, demographic glaciation, and the race for renewable energy, there are more thorns and sharper that among the impenetrable brambles that surround the enchanted castle. In fact, in many ways the context refers to the original version of the fairy tale of the same name, that of Giambattista Basile, rather than the sweetened plot of Charles Perrault.

However, we can see a glimpse of a European economic revival. There are encouraging signs. Strong and weak signalsAmong the strong was theunexpected increase (to the extent) of GDP in the last quarter of 2025: +0,3% in the Eurozone (+0,4% net of the Irish decline, due to the invoicing policies of large multinationals with registered offices in Ireland). Furthermore, the unemployment has started to fall again, equaling the low of thirteen months earlier last December. Finally, the orders to German industry They're back on track, especially the large ones, which at the end of 25 climbed back to the levels of four years ago; the others are still 13 percentage points below.

Germany in crisis…

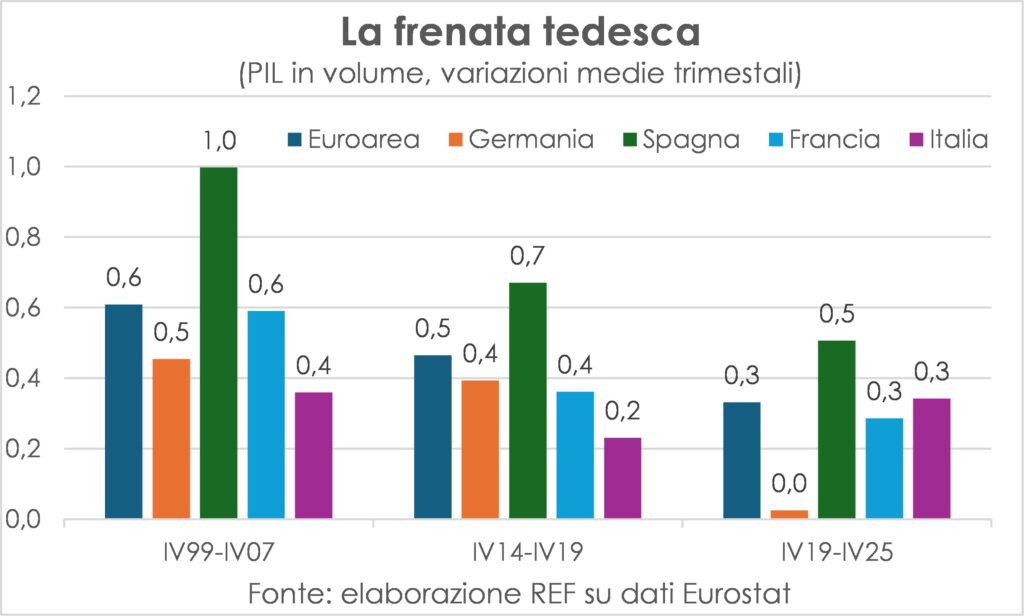

The trend in GDP in the period from the pandemic onwards reveals, if compared with two previous sub-periods (i.e. end of '99-end of '07 and end of '14-end of '19) that at the heart of European weakness is the German crisis; Germany's economic dynamics has almost collapsed, with variations visible only to the second decimal place (0,02% quarterly average), against the previous 0,4-0,5%. That crisis is based on theautomotive: the transition to electric has generated a wave of the famous Fear Teutonic at the top of the major German automotive causes, which are struggling to get out of the ford between internal combustion and EV. Furthermore, the energy intensive industries, another pillar of German industry; and the loss of output from these industries (-20% since the end of 2021) is likely to be permanent.

Fortunately, Germany understood a year ago the need to change the model and focus on domestic demand driven by public investments in infrastructure (including schools and hospitals) and armaments. Now that shift is starting to translate into spending and in fact to pull they are the internal orders.

…makes Italy appear dynamic

Compared to the German trend, theItaly from a tortoise it seems to have transformed into a hare. So much so that some people speak of change of pace. In reality, as we have seen, compared to both of the two previous sub-periods, the one that changed pace (backwards, however) was the rest of Europe,: from +0,6% and +0,5% to +0,3%, against +0,4%, +0,2% and +0,3% in Italy. Without the superbonus and public investments from PNRR Italian GDP would have increased as in the previous period, and perhaps less. It's true that exports and non-construction investments performed well, but the former were due to the two interrelated compressions of domestic demand and real wages, and those investments are visible everywhere except in productivity, to paraphrase Robert Solow. Finally, in Italy, the PNRR is nearing its end, but the government will avoid a collapse in public capital spending, following the guidelines indicated in the DFP (Public Finance Document) last April.

Confidence is on the rise

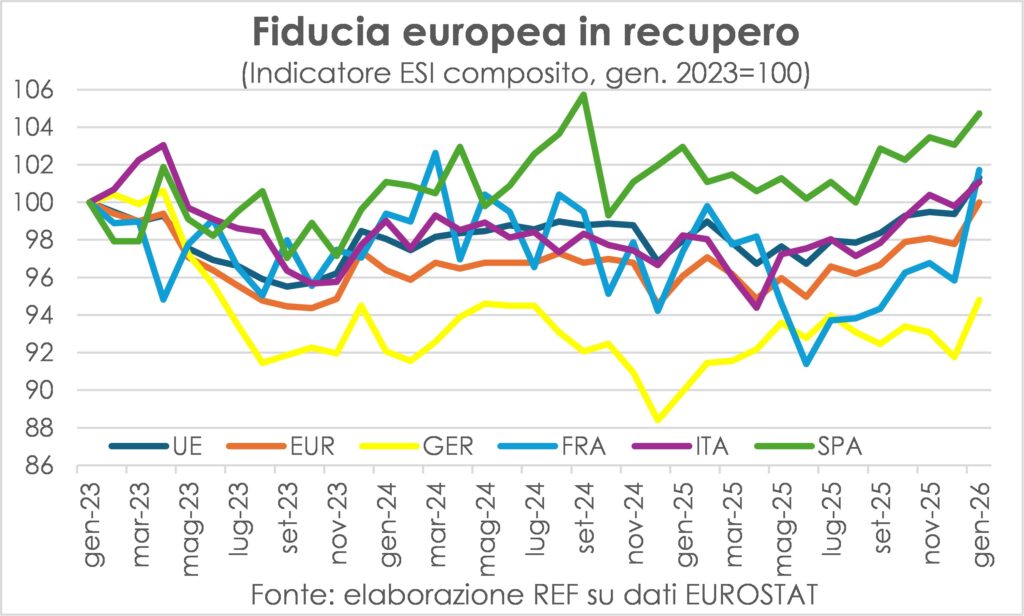

Among the weak signals that suggest that the European economic awakening is underway, the composite confidence of businesses and consumers, which rose to a three-year high in January, albeit with notable differences between countries, differences that reflect the different dynamics: Spain in the leadGermany trailing but rising sharply from year-ago lows.

Asia in choral growth…

Outside Europe, indicators for the beginning of 2026 (PMI in January) point to good, stable weather in Asia, where activity is improving in India, Japan and, to a lesser extent, China, and progress is being recorded in almost all other economies in the area or neighboring ones (South Korea, Australia, Vietnam, Malaysia, Indonesia, Thailand, Taiwan), confirming a collective momentum that reinforces each other; in fact, it is the only area where exports have started to increase again.

…while American employment starts growing again

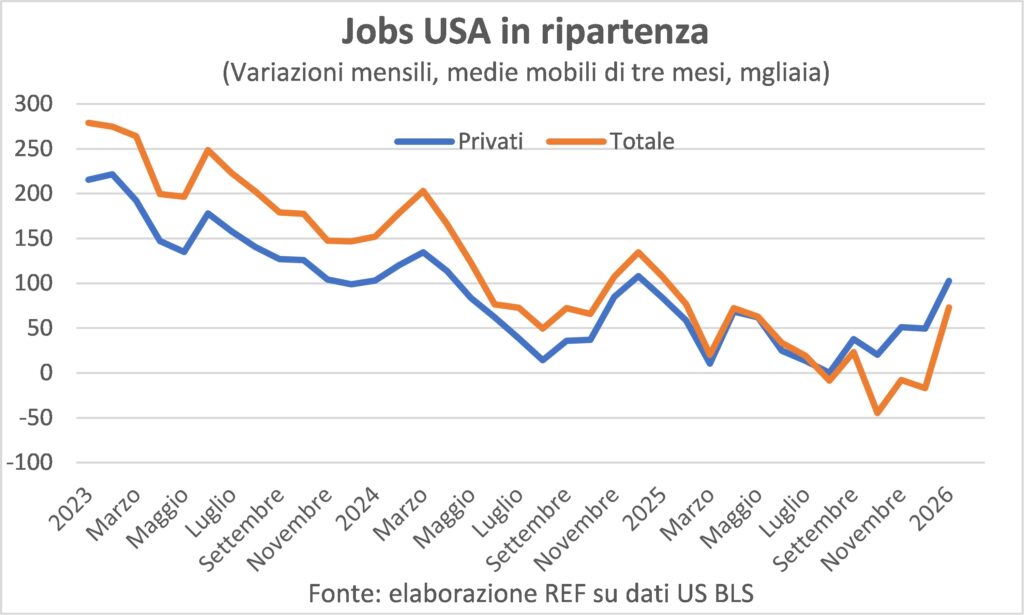

In USA there was a sudden brake on the retail sales in December, despite Christmas shopping appearing to have gone well. In fact, the consumers continue to be concerned about the shortage of new jobs and the nest egg of the accumulated savings during the pandemic it more than halved and its reduction has accelerated in recent months because the real wage bill remained unchanged for a long time during 2025. However, in the tug of war between a brilliant increase in domestic final demand and a weak employment situation, the former is winning: the creation of jobs in the private sector It reached its lowest point in August and in January it reached +103 thousand (three-month moving average).

Inflation cooling everywhere

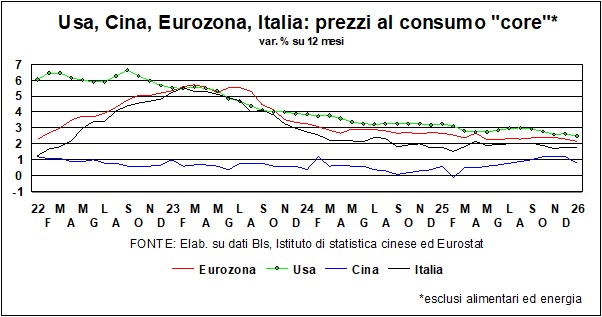

The inflation continues to fall, in different sizes and on both sides of the Atlantic and in Japan. While it has risen again in China leaving behind deflation (negative price variations), a symptom of weak demand and excess production capacity, and difficult for monetary policy to manage.

La Japanese inflection The annual change in consumer prices from 2,9% in November to 2,1% in December was "manipulated" by the introduction of new and higher energy subsidies. In fact, the annual change in consumer prices remained unchanged. core, which does not include energy and fresh food, at 3,0%; in January in the Tokyo area (a good predictor of the national trend) fell to 2,4% from 2,7% in December. So is the return to a more physiological trend in Japanese prices proving ephemeral this time too? A negative answer to hear the businesses, with manufacturers saying they have increased price lists in January at the highest rate in over a year and a half and with those of services they applied the highest increases in seven months.

In 'Euro area the annual change in consumer prices went from 2,1% in November to 1,9% in December to 1,7% in January. The decline in core is less pronounced: from 2,4% in three months to 2,2% last year, while in services it went from 3,5% to 3,2%. On the other hand, it is normal that in the tertiary sector prices remain warmer, because productivity gains are lower. Some forecast a further decline in annual inflation, based on the strong increases recorded in the first half of 2025, but even these analysts agree that the core inflation will remain around or above 2% and that the services sector is slowing down together with wages.

These disinflationary performances are, after all, ordinary, given the trend in the determinants of input costs (see below). Instead, the cooling of consumer prices observed in the United States, who seem to have ignored the sudden and widespread increase in import dutiesIndeed, the annual rate of change increased slightly from 2,3% in March 2025 (the month before the new tariffs were announced) to 3,0% in October, then dropped to 2,4% in January 2026, but only slightly compared to the fears and forecasts that saw it at 5%. It can also be correctly argued that without the tariff increase, it would have fallen earlier to within the Fed's target (2,0%), or even below, paving the way for faster and more decisive interest rate cuts. The fact remains that inflation is also in retreat in the US.

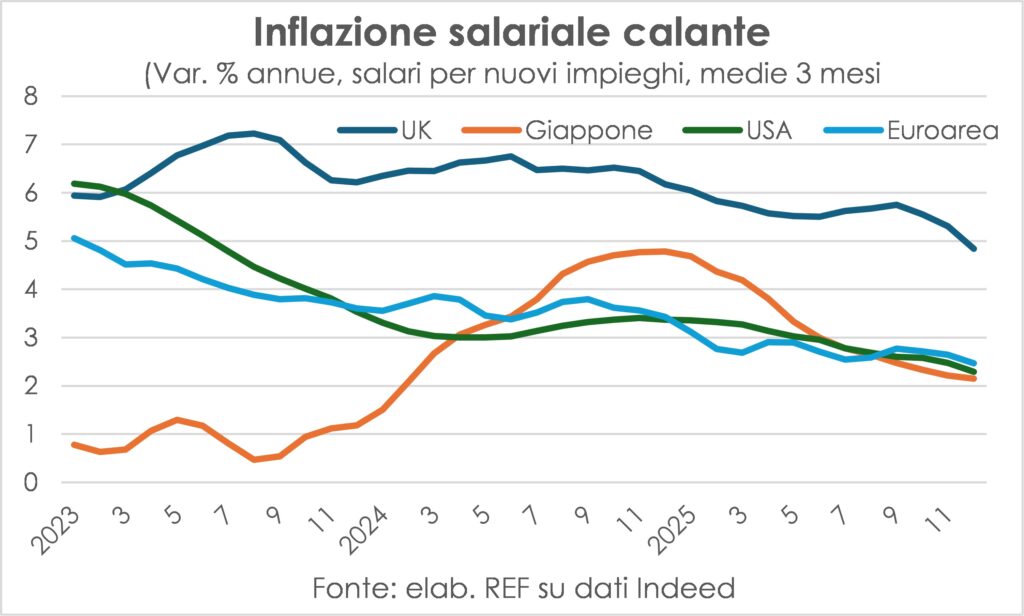

Wages slowly slow down

Already the wages, that is the cost of laborThey are the main variable in setting the tone for inflation, together with the productivity (two quantities closely linked). How are wages going? Are they... everywhere cooling albeit very gradually, also because the job market is increasingly on the side of the seller, with the great shortage of workers, even for the anti-immigration policies, with the exception of Hispanics.

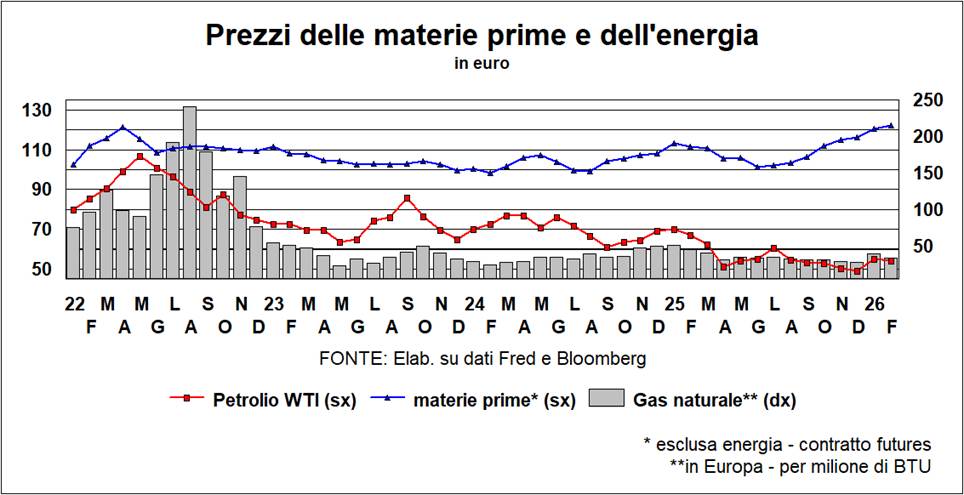

Le raw material, instead, behave in a diversified way: non-energy ones are rising, due to increased manufacturing activity and supply difficulties, while those of oil and gas fluctuate With winter temperatures and the reversals in US-Iran and US-Russia negotiations, all in all, they're neither pushing consumer prices up nor down.

The effects of artificial intelligence

In the more or less near future theartificial intelligence will act, like all technological innovations, as deflationary forceA supply-side deflation, that is, a good one, at least until the army of those left behind is so large as to compress wages and demand. A scenario that is now realistic.

(Very) long yields have stepped up their game

As already observed, there are many powerful reasons that explain, since the beginning of the decade, the rise of 30-year long-term yieldsThese yields are influenced by the cycle, which can suggest low rates when the economy needs a boost. The thirty-year horizon looks at the structure more than to the economic situation, and sees those pressures on public budgets that are there and will be there for a long time: state spending on infrastructure, For transitions environmental and digital, for the defense… Expenditures that affect all or almost all countries, and therefore extend across space and time, ensuring that, in the communicating vessels of international finance, the hunt for long-term funds continues and will continue. Of course, one should not exaggerate the length of maturities. There are those, like Alphabet, who are considering a 100 year bond, even if only for modest amounts. But 100 years is too long for a buyer, unless it's a pension fund that needs to pair its very long-term bonds with equally long-term guaranteed returns. Austria issued a 100-year sovereign bond, taking advantage of the low interest rates of the pandemic, and it's now trading at 20% of face value... (Of course, if it had been issued with high interest rates—but the issuer would have been ill-advised—things would have turned out differently...).

The hunt for funding is especially intense now that, at least in America, big tech companies need several billions to finance the huge investments in Artificial IntelligenceThe equally huge profits are not enough for these investments, and the market is preparing to provide the funds, even if there are many question marks: from doubts about the return on these investments to circularity of many deal, a circularity that could amplify the problems once doubts thicken…

It should be noted that, in America, the interest rate on thirty-year mortgages – a key rate for the American Dream of homeownership – has recently declined more than we would have expected from a parallel comparison with the T-Bond at 30 yearsIt is unclear how much of this is due to high demand factors. bond (Trump ordered public agencies Fannie Mae and Freddie Mac to buy $200 billion in housing bonds) or low housing prices.

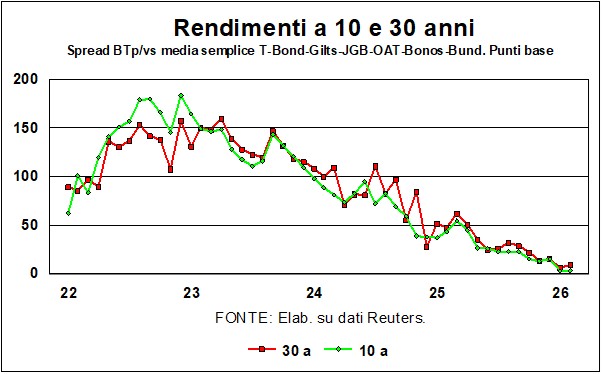

Coming to our house, we are comforted by the fact that the 30-year BTP yields They performed better than the others, in the sense that they grew less, didn't grow at all, or even decreased (depending on the starting point). The graph tells us that it's not just the spread with the Bund that has fallen: both in the 10-year and 30-year government bonds, the spread has gone down (see graph) compared to the average of the main stocks analogues (T-Bond, Bund, JGB, OAT, Bonos and Gilts).

This means that the trust the markets are placing in Italy also extends across space and time. And our spreads they still have room to go downThe decline in 30-year bonds is significant: it means that the markets see a more stable Italy in the long term, they do not fear relapses into easy finance or the temptations of inflation or political instability or worse (the cover of "Der Spiegel" – spaghetti and guns – during the dark years of terrorism is a distant memory...). Let's take the French case: the spread between BTp and OAT, which had even gone negative (partly due to our merit, partly due to French demerit), has risen towards breakeven on the 10-year maturity, after the French government narrowly managed to secure a yes to the budget, abandoning plans to put its social security accounts in order. But this spread still remains negative in the 30sFrance has bigger public debt problems than Italy…

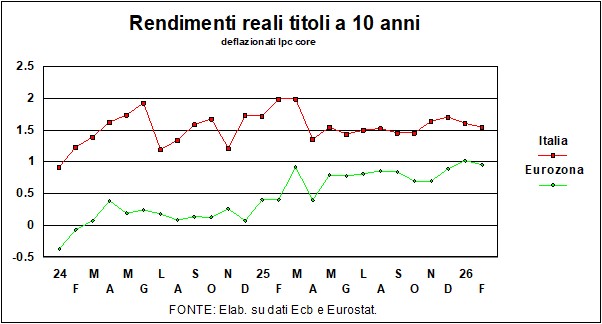

As noted in the past, the returns that matter for the growth of the economy are those Really. Italy suffers, for good reasons (inflation is among the lowest of the 21 eurozone countries), from a real rate higher than the Eurozone average (see graph), and higher than the economic growth rate (hoping that the second will approach the first...). But even here the reduction of the spread helps usAs can be seen, the gap between our real rate and that of the Eurozone has narrowed.

And now we come to the short-term maturities, and in particular to the key rates. Central Bank of Australia It was the first to reverse the direction of rates, and raised them (to 3,85%), after the inflation rate (also core) was confirmed (at 3,80%) above the 2-3% target. Also the Fed, in theory, is in the same situation, with inflation above the 2% target, but there is no chance that it will raise rates: the markets see a moderating price dynamic and a real economy dynamic that is not overheated, and they are only worrying about timing of the next cut, perhaps in June or July. The date is not indicated by chance: it would be the first decision under the new Fed Chairman. Kevin Warsh, assuming that the nomination of the chosen one is confirmed in the Senate, where a Republican senator (who has nothing to lose, since he has already said he will not seek re-election) has repeatedly announced that he will not give the confirmation vote until the issue is resolved grotesque story of the indictment of Jerome Powell by the Trumpian Department of Justice.

No cuts in the near future on this side of the Atlantic either: ECB, with a key deposit rate of 2%, calm inflation (and stable in the "core" version) and a recovering economy, can afford to leave the rates where they are.

Dollar weak, Yen and Yuan strengthen

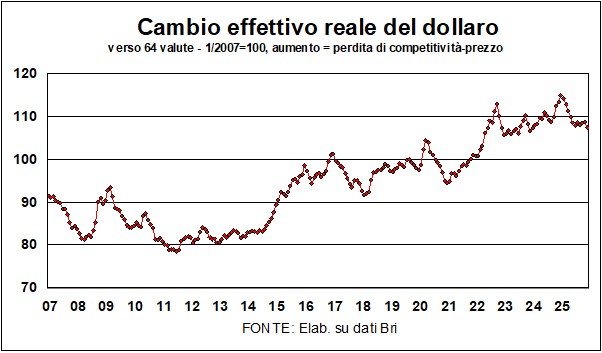

We have already argued in the past that, if the Trump Administration strongly wants – as it says and repeats – to reduce the trade deficit, there are no possible scenarios that do not include a dollar decline. The duties – it's now clear – they are not the right weapon. The main roads are – alternatively or jointly – or one recession that permanently cuts domestic demand or a dollar that weakens to the point of increasing import prices and stimulating exports. Since a recession is politically unadvisable, the weak dollar.

In fact, if we look back over the past twenty years, the dollar has room to fallIts real effective exchange rate – see chart – is still uncomfortably strong. At the beginning of 2025, its loss of competitiveness, compared to the average of the first decade of the period, was about 25%. Now the loss has reduced to about 17%, but the American currency still remains uncompetitive. Perhaps this is why Trump he said he wasn't worried about the falling dollar (though his Treasury Secretary later said Besent He tried to patch things up by repeating the hackneyed mantra of the 'strong dollar,' while Warsh talks about a 'healthy dollar.'

Lo yuan it's slowly happening appreciating, even towards the euro, to tone down the criticism of the rampant Chinese trade surplus. Let's get to the yenWe have already highlighted the anomalous weakening in the past, anomalous because it occurred despite the sharp decline in the interest rate differential between American and Japanese bonds. The latter have risen sharply and should have favored the yen's exchange rate. There are some signs of recovery and a weakening of the anomaly, with the yen having begun—and expected to continue—to strengthen.

Stock markets: 'Friendly fire' on Wall Street, growth elsewhere

Stock market legends tell that Joseph kennedy (JFK's father) worked on Wall Street as stockbroker in 1929, and took a break to have his shoes shined. The shoeshine boy, on the sidewalk of that street, gave him some advice on which stocks to buy, at which point Kennedy Sr. decided that if even the shoeshine boys had entered the market, it meant that euphoria had taken over and the top was near. He returned to work, sold everything, and took down options. Shortly thereafter, he made a fortune…

The story – perhaps apocryphal – comes to mind when looking at how the daily stock trading on Wall Street: they have soared to more than a trillion dollars, doubling compared to a year ago. We don't want to scare anyone; almost a century has passed since then, but caution is warranted...

Since the arrival of theIA, both the educated and the illustrious continue to ask whether this innovation will wipe out jobs, how many and which ones? But what has happened in recent days is shifting the target. Wall Street is sagging under the 'friendly fire', meaning that many listed companies (in the software field but also in traditional sectors such as real estate, logistics, and asset management) have suffered serious losses. The ones opening the fire are the large and small AI companies, which are putting on the market products aimed at taking away customers from the above companiesCertainly, if the "civil war" were to continue, jobs would also suffer...

It has been sixteen months since Donald Trump He was elected President of the United States. What impact did Donald Trump's attacks on the international order have on financial investments?

Starting from the month before his election, and looking at four sizes – Gold, Stock Exchanges excluding the US, Wall Street and Bitcoin, expressed in a common currency, the dollar – let's see the following ranking:

- Gold, by far in first place, with an 85% increase. The yellow metal has experienced (due to the aforementioned setbacks) a new lease of life as a safe haven.

- In second place are the Ex-US stock exchanges: +34,6% (with Japan, Italy and Germany leading the way).

- In third place, Wall Street, with a +20%.

- Last, the Bitcoin, which fell below its initial level: -5%.

Bitcoin's bleak performance does not surprise us, given our atavistic aversion to the world of cryptocurrencies, which we have always defined as 'a solution in search of a problem'. More surprising – we have already noted – is the fact that the The American stock market has performed worse than the rest of the world, despite the fact that America is at the forefront of the AI innovation wave and that Trump's tariffs were supposed to benefit the US and harm non-US countries. As already mentioned, better to diversify…