- digital tools they are increasingly part of our lives: we communicate via email and messaging apps; we book our trips with a few simple clicks on the internet; we compare the prices of products and services on specialized sites; we keep our photographs, in the form of sequences of bytes, on our smartphones; we read books in digital format; and so on.

Digital euro: why?

It is quite natural that this tendency to digitization manifest itself also in the world of payments: when we purchase a product on a website and have it delivered to our home, or when we place our smartphone on an electronic reader in a shop, we are paying with a digital tool. And we have been doing it for years now: those gestures have become part of our habits.

What is a digital currency issued by the Central Bank for?

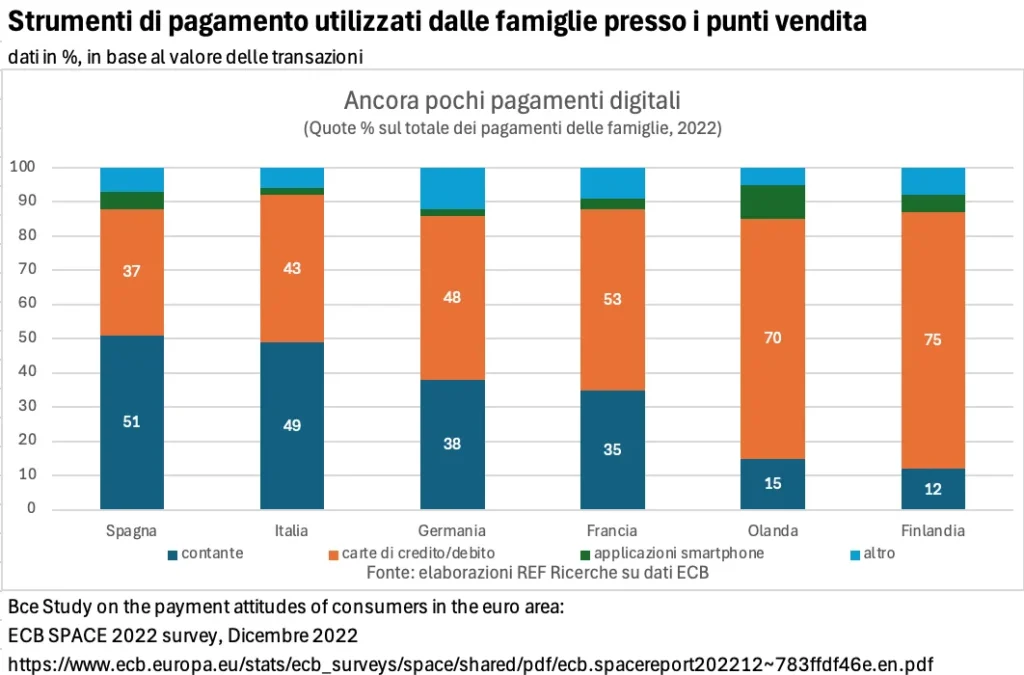

The use of digital means of payment was greatly accelerated by the difficult phase of the lockdowns imposed by the Covid-19 pandemic, when the closure of many physical sales points gave impetus to online commerce; at the same time, in the commercial activities that have remained open, the use of electronic payment cards has significantly increased, often used in contactless mode. These trends, which already started before 2020, have continued in more recent years: between 2019 and 2023, the share of expenses made in Italy with the digital payment instruments most frequently used at the point of sale (debit, credit, prepaid cards ) rose from 24 to 35 percent; the increase was particularly intense between 2019 and 2021, when, in addition to various restrictive measures imposed to stem the Covid-19 pandemic, the standards times a boost the use of digital payment tools. The convenience of payments made with digital tools is evidently exerting an increasingly strong attraction towards Italian consumers. Similar trends, if not more accentuated, are also observed in other European countries.

The spread of digital technologies has also favored the development of new financial products, known by the name of crypto-assets. In many cases, these are extremely risky instruments, the value of which can undergo extreme fluctuations, as illustrated by Riccardo De Bonis in the contribution published in this Guide on 27 July.

Digital euro: what?

In this context, many central banks have started to consider the idea of issuing, alongside cash (banknotes and coins), a digital currency (CBDC, acronym for Central Bank Digital Currency) at retail, which would allow for meeting the changing preferences of users and would provide at the same time a payment method both in step with the times and absolutely sure.

Among the reasons behind this trend there is also the awareness that, if the demand for digital payment instruments is not satisfied by local authorities, it could end up turning towards digital currencies issued by other entities, for example large technological operators (the so-called BigTechs) or other central banks, which would naturally take care to safeguard only their own interests and the functioning of their own system. Issuing a digital currency would therefore allow a central bank to protect the public interests associated with the value of the currency, thus safeguarding the monetary sovereignty as well as the integrity and reliability of the payments system and therefore, ultimately, also financial stability.

The possible issue of is also included in this context a digital euro by the 'Eurosystem (at the moment, the decision to proceed in this direction has not yet been formally taken; in order not to unnecessarily burden the text, from now on we will avoid reminding at every turn that the issuance of the digital euro is currently possible but not certain).

The digital euro, if issued, will be the digital equivalent of cash

The digital euro would also be one digital version of cash, which it would join without replacing it and with which it would share the main characteristic: that of being a liability of the issuing institution (of therefore being, ultimately, "guaranteed" by the latter), in this case of the Eurosystem . It would therefore not be a question of duplicating electronic or digital payment instruments that are already available or will be available in the future: none of those instruments will ever be able to possess the same reliability and security requirements that the digital euro would enjoy.

With the arrival of the euro in digital format, the currency would change once again leather. This is nothing new: paradoxically, one of the constant characteristics of money has always been change. It is possible that the introduction of the digital euro will initially be greeted with doubts. But this wouldn't be anything new either: when, after centuries of exclusive use of metal coins, the first banknotes printed by issuing institutions began to circulate in mid-eighteenth-century Italy, this payment instrument, which to us today appears completely obvious , initially met with some skepticism. So much so that, several decades after the first appearance of paper money, Giacomo Leopardi he still deplored the fact that in his time «it was […] customary to sell and buy […] not with gold and silver» but that, on the contrary, «civilized peoples […] were content with policies for money» (« Dialogue of a Goblin and a Gnome", in "Moral Operettes", written exactly two centuries ago, between 2 and 6 March 1824). The Bank of Italy, in concert with the European Central Bank and the other central banks of the Eurosystem, will implement a range of communication activities to ensure that potential users can always count on correct information regarding the importance and functioning of the digital euro as well as the benefits it could bring to their daily lives.

What features will it have and How will the digital euro work?

Digital euro: how?

If issued, the digital euro will be usable for different use cases and on different technological supports. All necessary measures will be taken to ensure safety, including with regards to cyber risks, and to contain the risks of side effects.

Given that some characteristics, even not insignificant ones, have yet to be fully brought into focus, it is certain that, just like its paper alter ego, the digital euro will allow carrying out, at any time and in any place in the area of 'euro, transactions e payments towards all the main categories of economic subjects: consumers, businesses, public administrations. Private individuals will be able to make purchases at physical or virtual sales points and make payments to other private individuals; both companies and citizens will be able to receive payments from and make payments to public administrations. However, the possibility for companies to make payments to private individuals or other businesses will be excluded, at least in a first phase, just as completely automatic payments will not be possible, initiated for example between machines without human intervention and on the occurrence of certain conditions.

Payment methods and environmental impact

Payments can be made in both ways online – when a network connection is available and it is therefore possible for intermediaries to validate the transaction – both in mode offline – when, on the contrary, there is no connection or the offline mode is preferred by the parties. In this case the transactions would be recorded only on the devices of the counterparties involved; personal data from offline payment transactions would therefore only be known to the payer and the beneficiary, offering users a level of privacy similar to that of cash. The maximum will be guaranteed in both cases of your digital ecosystem. of the transaction, also with respect to risks of nature cyber.

Among the non-secondary objectives of the digital euro project will also be that of containing theenvironmental impact compared to existing payment instruments. By way of example, according to an ECB study, the pollution produced by payments made in a year by a person using euro banknotes is equivalent to that generated by traveling eight kilometers in a medium-sized car. The adoption of adequate design measures in the development of the digital euro will make it possible to significantly contain energy consumption.

Promote financial inclusion and ensure privacy

Particular attention will also be paid to promoting thedigital financial inclusion, taking care that - in line with its public nature - the digital euro is available to every citizen even if they are not "banked", i.e. not active in banking and financial circuits, or without technological capabilities or suffering from disabilities. Other characteristics of the digital euro will also be designed taking into account the indications emerging from the dialogue that the Eurosystem has started some time ago with a plurality of subjects, representing different categories of economic agents, in order to detect the preferences of the latter. Among the themes that emerged during this dialogue was the request to guarantee a high level of privacy, while at the same time avoiding the use of the digital euro for illicit activities. The digital euro will therefore be designed in such a way as to guarantee a level of privacy higher than that usually offered by other digital payment methods.

If and when digital euro will be issued, euro area citizens will be able to own digital wallets, offered free of charge for basic functionality and accessible via payment card or smartphone app, in which to hold their digital euros.

Security and risk management

However, appropriate safeguards will be adopted to prevent phenomena of excessive reduction of costs from occurring with the introduction of the digital euro. bank deposits, due to which banks may have to resort to more expensive sources of financing, or reduce the loans granted to productive companies, with negative repercussions on the financing of the economy and on financial stability. To this end, for example, constraints could be imposed on the quantity of digital currency that can be held by the individual user.

To ensure that compliance with these constraints does not compromise the digital euro payment experience, the user will be able to activate, for online transactions, technical functionality (cd waterfall/reverse waterfall). In the presence of these functions, if the receipt of a payment in digital euro causes the maximum holding limit to be exceeded, the excess amount will be automatically transferred to the bank account possibly connected for this purpose; similarly, if a user wanted to make a payment for an amount greater than their available digital euro, the missing amount would be automatically withdrawn from any connected bank account. It will also be possible to set up an automated funding/defunding function on a voluntary basis, to automatically transfer funds from the digital euro account to the bank account or vice versa, upon the occurrence of specific conditions defined by the user, such as exceeding the amount of euros digital desired by the user himself.

Digital euro: when?

The Eurosystem has started it studio of the possible European digital currency already four years ago and is preparing to be ready for its issuance, when the necessary conditions are met and the decision is eventually taken.

The digital euro project does not only involve the Eurosystem. The European legislator is simultaneously preparing the legislative provisions needed to provide the digital euro with the necessary regulatory support. The decision on the issuance of the digital euro, which will be solely up to the Governing Council of ECB, can only be taken after thelegislative process will have come to an end. In the meantime, the Eurosystem is working intensively to ensure that everything is ready for that moment, if and when the issuance takes place.