Economics and finance students are told that there is magic in financial markets where multitudes of subjects transfer huge funds to other subjects they do not know, even though they believe they have intangible rights to the repayment of funds, if anything increased by a return. If we replace magic with trust, we find the indispensable condition for the correct functioning of the financial markets. What is certain is that, as in the case of our country, no letter of intent can bring back the magic that has dissolved on the markets.

The recent proposal put forward by Michele Fratianni (published on Firstonline last October 25) in favor of the forced transformation of short-term government bonds into ten-year BTPs. Proposal that not only retrieves old tools (never used since the post-war period) from the toolbox placed in the attic for some time, but also expressly recalls the consolidation of the Italian public debt implemented in 1926 by Mussolini, which was followed by the impossibility for many years of power place new government bonds with enraged savers, and the deep recession of the Italian economy also due to the achievement of "90 quota" (G. Carli, G. Carli , Cinquant'anni di vita italiana, Laterza, 1993, pp. 20 -21). The magic had dissolved for a long time and with it the growth of the economy.

It is therefore worth remembering again Guido Carli (a great friend of Bruno Visentini) and his animated discussions (in the eighties and early nineties) with his friend at the time when, Carli recalls, Visentini's words, "stripped of the verbal artifices , always led there: to the forced restructuring of the public debt” . But Carli also reminded his friend that "operations of this type are possible only in a regime such as the one that allowed the massacre with sticks in the center of Rome, in via Crispi, of a person as valuable as Giovanni Amendola" (G. Carli , op. cit. p. 386).

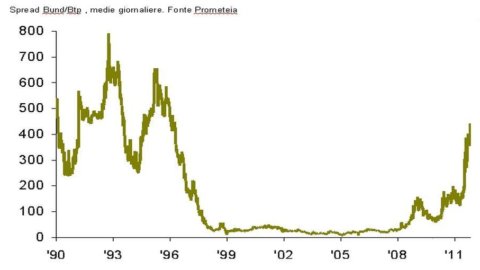

Having therefore discarded the hypothesis of a return to Mussolini's type of dictatorship (also because, unlike then, the euro replaced the lira and the ECB replaced the Bank of Italy in its function of lender of last resort), one could ask whether given today's conditions (a debt/GDP ratio of 120%; a level of interest rates which continuously fuels interest expense; a spread - see attached graph - between the Bund and the BTP which reflects, as it always has, the judgment of the financial markets with respect to the governments' ability to honor the debts assumed), it is appropriate to take the road of the administrative route (of which consolidation is the maximum expression) for the management of the stock of Italian public debt in replacement of the market route, while bearing in mind that today the average life of Italian public debt securities (calculated as at 30 September 2011) is 7,11 years and that BOTs at the same date constitute 8,93% of the stock and BTPs 64,73% of the same; albeit with an emission of colossal amount in 2012, as known to all but not to the Italian Government.

Maybe an exit from the Euro is recommended (the inevitable consequence of the consolidation of the public debt) as Paul Krugman also seems to want to suggest (International Herald Tribune of October 25th), supporting the wish of big US finance to be able to return to arbitration between multiple currencies competing with each other.

In any case, as the BIS - Bank for International Settlements reminds us "in principle, government intervention should be rapid and decisive with the clear objective of dispelling any uncertainty" (BIS, Report 2008. p. 161). But the subsequent experiences of these years show that neither the most noble European governments, nor our government, have been quick and decisive in their interventions to dispel any uncertainty and bring magic back to the markets.

But Fratianni's proposal allows us to reflect on our past: in the sense that we seem to hear the echo of the debate which, however excluding any hypothesis of debt consolidation, preceded the divorce in 1981 between the Treasury and the Bank of Italy (instigated by Andreatta and Ciampi) who, by exempting the central bank from guaranteeing the full placement of the securities offered by the Treasury at auction, sanctioned the separation of responsibilities between the legislative, executive and monetary powers in the management of the public debt and marked a radical change in monetary policy for the Italy's financial stability.

Going along the avenue of recollections, one also finds the proposal for a (non-administrative) fiscal policy that would incentivize investors to subscribe government bonds with longer maturities on the secondary market through very high rates on short-term bonds and rates equal to zero for securities with a ten-year maturity and beyond. The Treasury would have lost revenue against the advantage of the extension of maturities. It is obvious that this incentive, as was observed at the time, can only have an effect if the composition of household portfolios and the decisions of professional investors are inclined to evaluate the return on the security after tax; if, on the other hand, the yield on the security were valued gross of tax, the incentive would not have worked and the Treasury, in addition to not collecting the taxes, would not even have enjoyed the reduction in interest expense. In the midst of uncertainty, this road too was abandoned and today it seems inappropriate to try to bring it back to life due to the opacity of the contracts and financial instruments that the most famous professional studies could suggest.

Still on the avenue of recollections we meet 1992 during which the spread (see attached graph) moved between a minimum of 464 basis points in the first quarter of 1992 and almost 700 basis points in the fourth quarter of the same year (it will reach a minimum of 23 basis points in the first quarter of 1999). For its part, the debt to GDP ratio was 105%, rising rapidly towards the 120% it reached in 1994, as it is today. Everyone remembers that in September 1992 the lira left the EMS exchange rate agreements despite the measures adopted by the Amato government in July 1992, followed by the maxi maneuver in October of the same year. However, even then there was no hypothesis of returning to the administrative management of the public debt; the succession of credible governments both domestically and internationally was enough to bring Italy into the Euro, which in turn brought the Italian economy back on the path of financial stability and with it the magic on the financial markets.

Finally, a light version of consolidation could be found once again in the old toolbox, using the policy of portfolio constraints for the most diverse categories of investors. Difficult if not impossible path to take considering that foreign investors hold over 50% of the Italian public debt. As in 1926, the consequences would be disastrous for subsequent issues of Italian public debt securities.

There are no shortcuts – such as administrative solutions – to public debt problems. Likewise, it is not advisable to retrace the avenue of memories to rediscover old tools. All that remains, therefore, is to return to today's politics and its responsibilities, taking up the words of J. Schumpeter to this end, namely that the budget "is nothing but the skeleton of the state stripped of all fallacious ideologies (...) and that history taxation of a people is an essential part of its general history” (J. Schumpeter, State and inflation, Boringhieri 1983, p. 193).

Rediscovering the contents of the toolbox in the attic is never something a country can pride itself on, but even in this case the same tools would fail if the government did not appear quick and decisive with the clear aim of dispelling any uncertainty. The solution to problems, whatever the tools and the revisited box, therefore returns to the hands of politics.

If we look at the attached graph, we conclude that the policies that brought Italy into the Euro constituted a turning point in the general history of Italy, which unfortunately was not followed up. It seems trivial to repeat it, but the magic that has dissolved can only return with a policy that wants and knows how to imprint a new turning point in the general history of Italy with absolute internal and international credibility. Will our heroes (so to speak) of today be able to bring the spread back to no more than 23 basis points?