«Nothing new on the pricing front», an Eric Maria Remarque would have written as an economist. And the metaphor also fits into the profound content of the ending of the novel about the Great War. Just as then the death of yet another soldier could not make the news after 9.999.999 fallen, today, after years of price dynamics closer to 1% than 2%, it does not deserve to make big headlines on inflation that does not exist And.

A inflation-zombie, in the sense that she is dead but many see her ghost. In the Neapolitan grimace, 48 is «'o muorto che pparla». A dead man who appears in a dream to the nostalgic sleeper of the loved one who is no longer there. And in the end it is well understood that it is possible feel nostalgic for a little inflation, which would oil the mechanisms of the economy and help reduce the real cost of money.

Another thing, however, is to fear that ghost as one threat of future upheaval caused by the imprudent central banks that flood the world with money, finance the astronomical public deficits hands down and cancel the financial income. 'Euthanasia of the rentier,' Lord Keynes called it; a good death for everyone else, except the rentier himself? Depends: If the economy were left to run itself and experience a depression, accumulated savings would be destroyed in another way. For example, with a property, or with the bankruptcy of private and public debtors. In short, much more violent deaths compared to the sweet one of low rates.

A great economist, Olivier Blanchard, explains well why the return of inflation is a lot unlikely, with a lot of unemployed workforce and a lot of unused production capacity. For there to be inflation, Blanchard believes, three conditions must be met, of which the third is the one that really matters: central banks subservient to governments. Populist governments, he underlines. But precisely monetary expansion serves to prevent the health crisis that has become economic from turning into a social and political one, Weimar Republic style.

Maybe one day there will be more inflation, and maybe even hyperinflation, but it's still a distant day and before then who knows what will happen in the economy, and before that in society. "There are more things in heaven than on earth, Horatio," Hamlet would admonish.

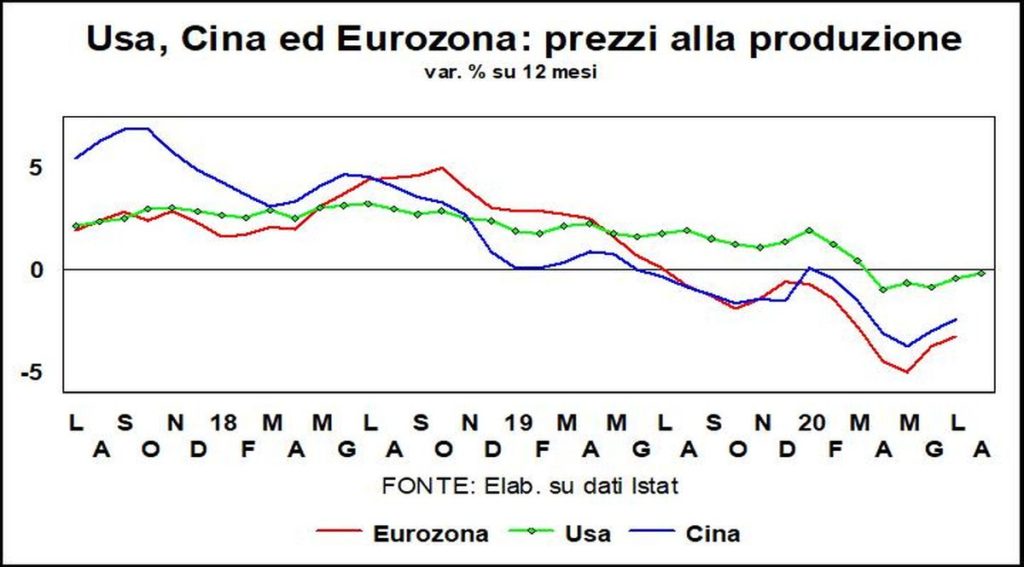

In here and now we find that the price momentum is cold, even with freezer temperatures. Both for consumption and for production.

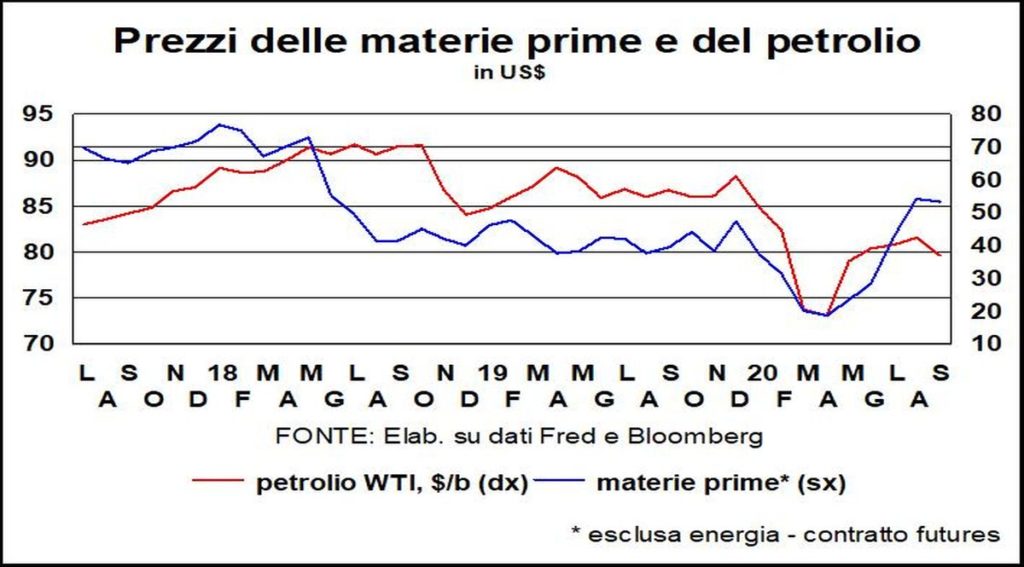

The quotations of raw material they have risen from the lows. Non-oil ones even above the levels of the end of 2019.

And in fact i costs for businesses go up, say the purchasing managers, but it is a limited increase and which is not transferred to the final prices except in a minimal part, because the competition is strong and is accentuated by thetechnological innovation in commercial distribution. Which is another nail in the inflation coffin.

Another issue is the effect of exchange movements on inflation. The ECB is trying to talk down the euro. Now it is true that an appreciation is equivalent to a monetary tightening (of variable entity according to the characteristics of an economy), because it subtracts net demand from domestic production via relative price movements, and that no one can afford to reduce the monetary stimulus. But other than that global value chains have greatly reduced these effects and that in advanced markets you compete more on quality and innovation than on prices, the impression is that the central bankers gathered (albeit virtually) in Frankfurt are unable to free themselves from personal and national history, when "beauty shines in their eyes” and reasoned in terms of medium-small countries and very open to trade with abroad. Now with the European Union so integrated (even without the UK) and which finally wants to relaunch itself through internal demand (moreover, since trade with foreign countries is always scarce, due to Covid-19) reasoning like this is like driving looking in the rear view mirror. A euro at 1,18 or 1,25 would not change much in the (de)flationary scenario we face.