Also this year the appointment with the "multi-purpose communication", better known as "spesometro", one of the main anti-evasion tools in the hands of the Revenue Agency is back. The basic principle is that VAT payers are required to communicate to the tax authorities electronically the transactions relevant for tax purposes carried out during the previous year, but there are many distinctions and details to take into account .

1) WHAT OPERATIONS ARE THEY INCLUDED IN THE SPESOMETER 2016?

The 2016 spesometer must contain:

– all transactions with an invoice obligation, regardless of the amount;

– transactions without invoice obligation for an amount equal to or greater than 3.600 euros (gross of VAT);

– transactions in which the invoice was issued in lieu of another document, regardless of the amount;

– operations subject to reverse charge (a particular VAT application mechanism in which the tax liability is shifted from the seller to the buyer) for which VAT has not been charged on the invoice;

– transactions subject to the split-payment (the split payment mechanism with which the PAs pay the VAT directly to the Treasury and not to the supplier).

2) AND OPERATIONS EXCLUDED?

In general, in the 2016 survey it is not mandatory to communicate the operations already monitored by the Revenue Agency. Here is the list:

– VAT exempt financial transactions;

– payments of an amount equal to or greater than 3.600 euros made by credit, debit or prepaid cards to taxpayers who are not subject to VAT (and therefore not documented by an invoice);

– operations already communicated to the Tax Registry;

– data already transmitted to the health card system (Sts), but the Revenue Agency specifies that "taxpayers can also indicate in the multi-purpose model of the spesometer the data already transmitted to the health card system if this is easier from an IT point of view" ;

– imports and exports of goods from and to non-EU countries already declared to Customs;

– transactions within the European Union subject to declaration for Intrastat purposes.

3) WHAT THEY ARE DEADLINES OF THE SPESOMETER 2016?

The deadline within which businesses and professionals must send notification of invoices issued last year originally varied according to the frequency of VAT payment in 2015 (April 11 for monthly taxpayers and April 20 for quarterly ones). But then the Revenue Agency decided to unify the deadlines: the date to mark on the calendar is April 20, a deadline valid for all taxpayers, both monthly and quarterly.

4) WHO IS IT EXEMPTED FROM THE 2016 SPESOMETER?

Several categories are exempt from the 2016 spendometer:

– lump-sum tax payers;

– minimum taxpayers (in the event that the right to the subsidized regime ceases to exist in 2015, it is mandatory to communicate the operations carried out from that moment on);

– public and autonomous administrations;

– retail traders for active transactions with a unit amount of less than 3 thousand euros (net of VAT);

– travel agencies for active transactions with a unit amount of less than 3.600 euros (gross of VAT).

5) HOW THEY ARE SENT THE DATA FROM THE 2016 SPESOMETER?

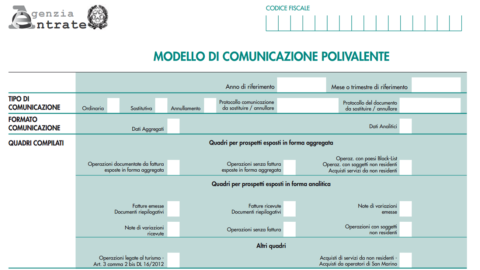

Communications relating to the 2016 spesometer must be made exclusively electronically (via fisconline o Enter) through the multipurpose communication model – pdf. You can choose between two compilation methods:

– analytical, specifying the individual invoices issued and received in the FE and FR parts;

– aggregated, using the FA part for the transactions documented by the invoice and the SA part for the others.

[Detailed instructions on how to fill in the document are available on the Revenue Agency website - pdf]

Furthermore, in the same multi-purpose model used for the 2016 spesometer, other data must also be indicated:

– transactions for amounts exceeding 10 thousand euros carried out by VAT payers with economic operators who have their headquarters, residence or domicile in countries included in the black list (the deadline for making this communication has been extended to 20 September 2016);

– purchases from San Marino by the last day of the month following the month in which the transactions were noted in the VAT registers;

– transactions relating to financial and operating leasing, lease and/or rental of cars, motor homes, other vehicles, pleasure craft and aircraft.