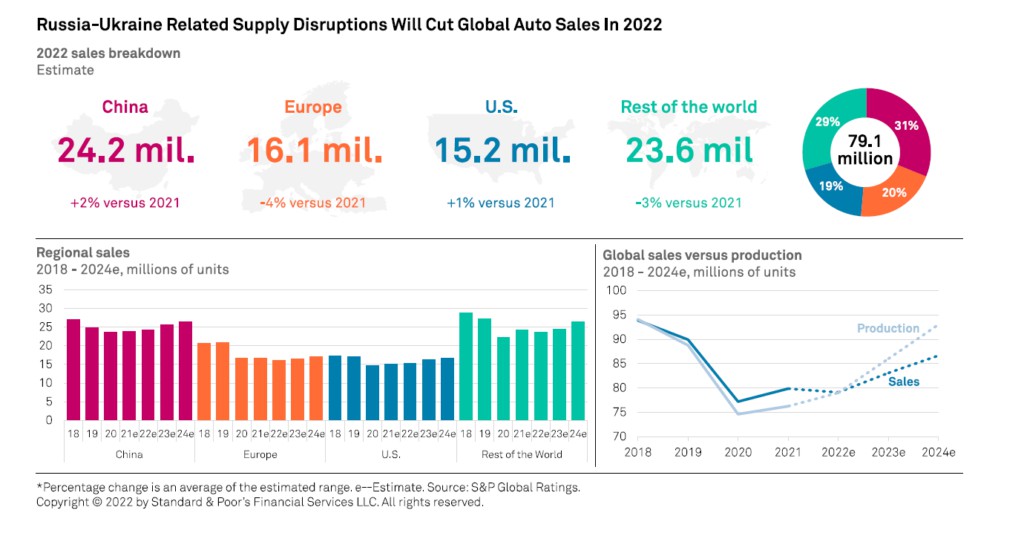

The war in Ukraine and related economic sanctions will have a negative impact on the world car marketespecially on the European one. This is what emerges from aS&P Global Rating analysis that for 2022 it expects a decline in the global car market of 2% compared to 2021 to 79,1 million units, when before the war the expectation was for a growth between 4% and 6%. The causes, the research explains, are indirectly linked to the conflict that has caused logistical and supply chain problems, shortages of critical vehicle components - including the production of wiring harnesses in Ukraine - and shortages of raw materials. Problems that add to a supply chain already under stress due to the pandemic and the semiconductor crisis. Either way, the agency expects EV sales to continue accelerating this year, to reach 15-20% of the global fleet by 2025.

In particular, S&P expects that in 2022 the auto market in Europe will record a decrease of 4% compared to 2021 to 16,1 million units. While the Chinese market – relatively sheltered from inflation – is expected to grow again by 2% to 24,2 million units. For the United States, the estimate is a growth of 1% to 15,2 million. For the rest of the world, S&P forecasts a 3% drop in sales to 23,6 million units.

Global auto market: logistics and supply problems

Disruption of the global supply chain and inflation due to raw material shortages are real risks for the automotive industry. Original equipment manufacturers (OEMs) based in Europe have suspended production at several plants. In particular, the disruption in the supply of critical automotive components from the region, including the production of wire harnesses in Ukraine, potential shortages of materials such as palladium and price increases of steel, copper, aluminum and nickel are key risks for the industry for 2022.

In addition, light vehicle production could struggle to surpass pre-pandemic levels in 2023, according to S&P analysts. The recent earthquake in Japan and the suspension of production at Renesas semiconductor plants pose further downside risks to the previous hypothesis of a more balanced supply and demand dynamic for chips by mid-2023. On the one hand, a gradual recovery on the supply side is expected, on the other hand, a brake on demand due to the rising cost of living, especially in Europe and the USA.

The critical issues in the supply

Energy supply disruptions or price shocks could also have ramifications for global auto production and demand. The conflict could have material implications for the European market due to its external dependence on raw materials, gas and oil. Not only is it unleashing unprecedented spikes in commodity and energy prices, but it will lead to prolonged uncertainty about how the European Commission will execute its Repower EU strategy to end Europe's dependence on Russian gas.

“Based on very preliminary estimates, this would create a short-term energy shortage, leading to rationing. Auto suppliers will find themselves having to replace Russian suppliers in a situation of supply shortage and high transport costs.

There are some short-term credit implications for some global auto manufacturers and suppliers. As global inventories remain at record lows, automakers are finding themselves having to fill orders with lead times that have never been longer. And throughout 2022, the automotive industry will continue to be dominated by supply problems.

The combined impact of marginally higher production volumes in 2022 and higher prices may not fully offset cost inflation. As a result, the agency expects to see pressure on margins and cash flow generation over the next two years. In this market environment, auto suppliers will continue to struggle to pass production cost increases beyond contractual agreements with automakers and will have to adapt to new trends, such as direct sourcing of semiconductors and raw materials.

The electricity market challenges the crisis

There may be weaker momentum for electric cars in 2022 and 2023 due to shock prices for nickel and other battery-specific materials that cannot be hedged, such as lithium. According to data from the EV-Volumes database, in the first two months of 2022, electric vehicle sales grew by 94% compared to the same period of 2021 in the 15 most relevant global markets, while total passenger car sales growth was flat .

In Europe, sales expanded by 35% against a decline of 4,3% for passenger cars. Electric vehicles now account for 20,7% of the light-duty vehicle fleet, and S&P analysts expect they will make up more than 30% in 2025. Momentum in China's new energy vehicle sales remains solid, buoyed by ongoing government stimulus and growing customer acceptance (sales of new EVs increased 155% year-over-year in the first two months of 2022 and account for nearly 18% of total auto sales).

In the United States, the combined market share of electric cars and plug-in hybrids (featuring both electric and internal combustion propulsion) hit 5,5% in the first two months of 2022 compared to 4,2% in the same period in 2021. Positive momentum consistent with the agency's previous forecasts that they will exceed 15% of the market by 2025.

Auto market: sharp cut in production globally

It will not be only the sales of the automotive sector that will suffer the effects of the conflict, but also the production. On Russian territory, several production plants have already stopped and over the next few months, as a result of the sanctions, production activities will continue on significantly reduced volumes compared to initial forecasts.

Analysis by the S&P Global Mobility agency confirms that, globally, it is expected a cut of 2,6 million units for 2022 and 2023 as regards the production volumes of the automotive sector, of which 1,7 million for the European market. Analysts expect a total of 81,6 million units produced during 2022 and 88,5 million units in 2023. Overall, compared to previous estimates, the new forecasts are 5,2 million units lower.

Falling demand, shrinking supplies and a worsening chip crisis threaten to cause a global vehicle production meltdown. Then there is another element unrelated to the conflict and which risks causing a worsening of the chip crisis in the short term. There new wave of Covid-19 cases in China it is causing blocks in industrial production in the north of the country where industrial areas of great importance for the semiconductor sector are located, such as Shenzhen and Changchun.