How does country risk change after the tumultuous events that characterized the North African Spring and beyond? The Sace Studies office offers a general and updated picture of the most important events that have occurred in various world economies, assessing the effect they could have on country risk. Each country is associated with a differentiated risk level (Low: L1, L2, L3; Medium: M1, M2, M3; High: H1, H2, H3) and a forecast scenario. Here is the June 2011 overview country by country.

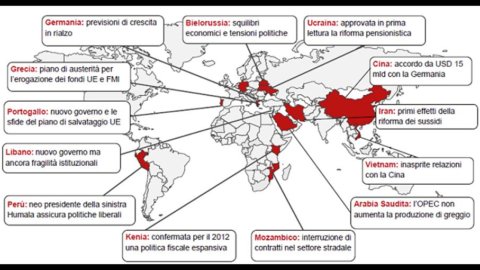

Saudi Arabia – Risk: M1; Outlook: stable

At the OPEC summit the member countries did not reach an agreement to increase oil production, which would have helped to lower its price and contain inflation. The increase in the production target of 1,5 million barrels per day proposed by Saudi Arabia and supported by the other Gulf countries, such as the UAE and Kuwait, has met with resistance from Iran, Venezuela, Ecuador, Iraq and Angola, whose trade balances are benefiting most from high crude oil prices.

Belarus – Risk: H2; Outlook: negative

In order to reduce the imbalances in the balance of payments, the government is planning a forced reduction of imports, a measure that would represent a violation of the agreements within the framework of the Customs Union with Kazakhstan and Russia and, consequently, could jeopardize the disbursement of tranche of the EurAsEc loan. Added to this is a growing discontent of the citizens, which since the beginning of June has manifested itself through repeated strikes and protests, resulting in the arrest of 450 protesters. The EU has tightened the sanctions against some Belarusian companies.

China – Risk: L3; Outlook: positive

Chinese Premier Wen Jiabao and German Chancellor Angela Merkel concluded a $28 billion trade and investment deal on July 15. The contract also includes a cooperation and research project between the two countries in the field of green technologies. The agreement implies complementary advantages for the two powers: China tackles the critical environmental issue by making use of German technology, leader in the sector; Germany confirms its position as China's main trading partner in Europe, with the possibility of using an educated and low-cost workforce for research on renewable sources, after the decision to abandon nuclear power.

Germany – Risk: L1; Outlook: stable

The Bundesbank has revised growth estimates for the German economy. After recording +2011% (short term) in the first quarter of 1,5, the economy should grow to 3,1% in 2011 and 1,8% in 2012. According to other estimates, growth could exceed 3% in 2011. Household consumption spending is growing, the rate of wage increases is accelerating and exports are expected to register an increase of 8,3% for 2011.

Greece – Risk: M1; Outlook: negative

The Greek Parliament has approved the implementing law of the austerity plan, a condition set by the European Union and the International Monetary Fund in order to obtain the new tranche of international aid worth 12 billion euros. The five-year austerity package plans to raise 28,4 billion euros in fiscal measures and spending cuts (14,1 and 14,3 billion respectively), in addition to 50 billion in revenues from privatisations. A vote that comes on the second day of the 48-hour general strike promoted by the unions and the indignados movement in a scenario of violent clashes between police officers and protesters.

Iran – Risk: H2; Outlook: negative

The IMF has expressed a favorable opinion on the effects of the subsidy reform adopted by the country, highlighting its effectiveness in the medium term. Despite the removal of 60 billion dollars of subsidies – equal to 15% of GDP – and the consequent general increase in prices, the authorities managed to contain the increase in inflation (from 10% in December to 14% at the end of May ). The objective of the reform is to abolish subsidies to energy sources and basic foodstuffs (in force for 30 years), on the one hand favoring a more selective redistribution of public resources and on the other the rationalization of energy consumption, in consideration of the strengthening of relevant international sanctions.

Kenya – Risk: H1; Outlook: positive

The budget for the 2011/12 fiscal year presented by Finance Minister Uhuru Kenyatta confirms an expansionary policy. Government spending is projected to be $13 billion, up 16% despite recent inflationary pressures and the poor performance of the agricultural sector. The budget includes an ambitious public investment plan in infrastructure (+36%), with the aim of improving in particular the supply of energy, water and ICT services. Against a 14,8% increase in revenues, the expected fiscal deficit for 2011/12 is 7,4% of GDP, up from 6% in 2010/11 and at odds with austerity plans announced a few months ago.

Lebanon – Risk: H2; Outlook: stable

The formation of the new government formally puts an end to the institutional deadlock, after 5 months of political vacuum. The opposition March 14 party has raised doubts about external interference in the appointment of the executive headed by Prime Minister, Najib Mikati, and dominated by the pro-Syrian coalition (March 8). The political situation remains fragile due to divisions between political forces. One of the main challenges for the government, in addition to initiating the necessary economic reforms, is linked to cooperation with the UN Special Tribunal on the murder of former Prime Minister Hariri. The investigations and the possible involvement of Hezbollah exponents close to the government could further undermine the political structure.

Mozambique – Risk: H1; Outlook: positive

The National Road Administration (Ane) is planning to terminate the contracts of 12 companies involved in the restructuring and management of the road network in the central province of Zambezia. The decision is motivated by the delays in the execution and the poor quality of the works, thanks to the inadequate supervision capacity of the local company Consultec. These problems are chronic and represent an obstacle for operators in the country. One example is the recent case involving the mining company Vale, which was forced to halt its exports of coal due to a delay in rebuilding rail links with the Moatize mines.

Peru – Risk: M1; Outlook: stable

The presidential elections decreed the victory of Ollanta Humala, a member of the nationalist left, over the candidate of the right Keiko Fujimori, daughter of the disputed president Fujimori, who is sentenced for human rights violations. Humala's proximity to the socialist left arouses concern in the markets, in particular on the future management of the country's mineral resources. However, the new president reiterated his intention to conduct liberal policies with greater attention to the weaker sections of the population, drawing inspiration from the political line of the former president of Brazil, Inácio Lula da Silva.

Portugal – Risk: L3; Outlook: negative

Pedro Passos Coelho, leader of the centre-right Social Democratic Party, is the new Portuguese prime minister. The Social Democrats won the elections with 38,6% of the votes and formed a government coalition with the ultra-conservatives of the CDS-Pp. The new executive will have the task of implementing the agreement signed with the EU, the ECB and the IMF regarding the three-year financial rescue plan of EUR 78 billion. The plan envisages measures to support growth, with the creation of new jobs, measures to consolidate the budget and stabilize the financial sector.

Ukraine – Risk: H2; Outlook: negative

On June 16, the Ukrainian Parliament approved the pension reform in the first reading. Final approval, which requires a second reading, is a necessary condition for the disbursement of the next tranche of financing by the IMF. The Ukrainian government expects the funds to arrive as early as the summer, however the objections to the reform coming from the opposition, which could require an examination by the Constitutional Court, should not be underestimated.

Vietnam – Risk: M3; Outlook: stable

Relations between Vietnam and China have recently soured due to the growing Chinese presence in the South China Sea. The Chinese government is accused of illegal exploitation of resources in the Paracel and Spartly Islands. The dispute, which also involves the other ASEAN members, has prompted Vietnam to seek support and involvement from the United States, which aims to strengthen its presence in Southeast Asia and counterbalance Chinese expansion. However, China remains a key partner for Vietnam, especially as an important export destination.

Attachments: SACE_country_risk_update.pdf