"Did you know that Does rhinoceros give great milk?». The question of the castaway Orlando (ironic and impertinent chronicler in Fellini's masterpiece E la nave va) helps narrate the final effects of the massive and continuous public interventions (including those of central banks) to support the economy. The beast-state, as liberal extremists see it, should do as little as possible. And even on this occasion we should let the economy fix itself, because we are only buying time, at the expense of future generations.

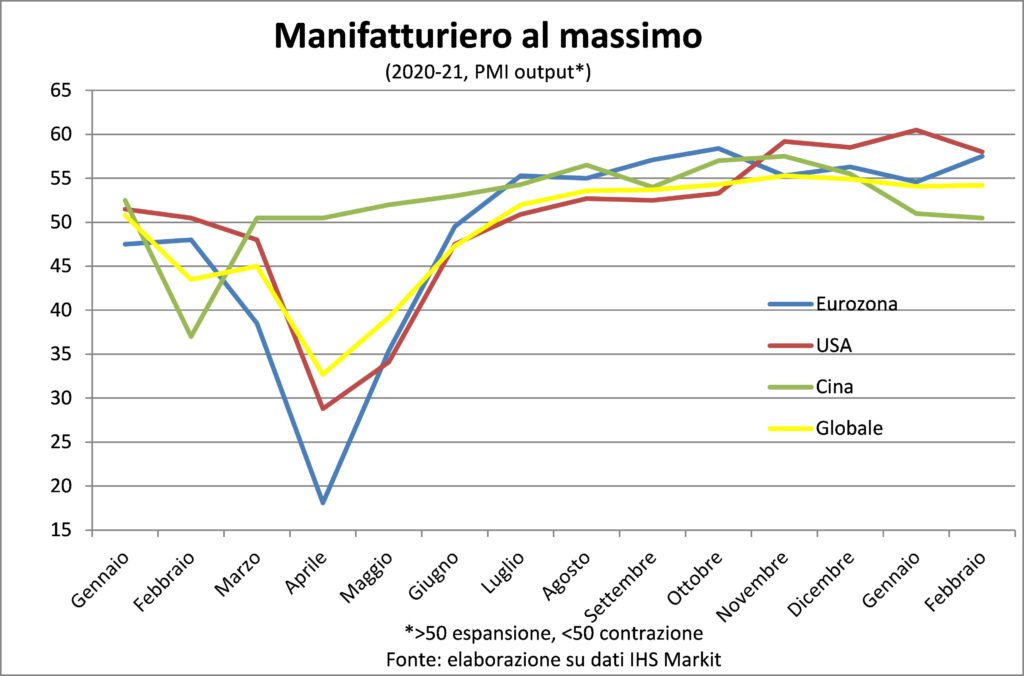

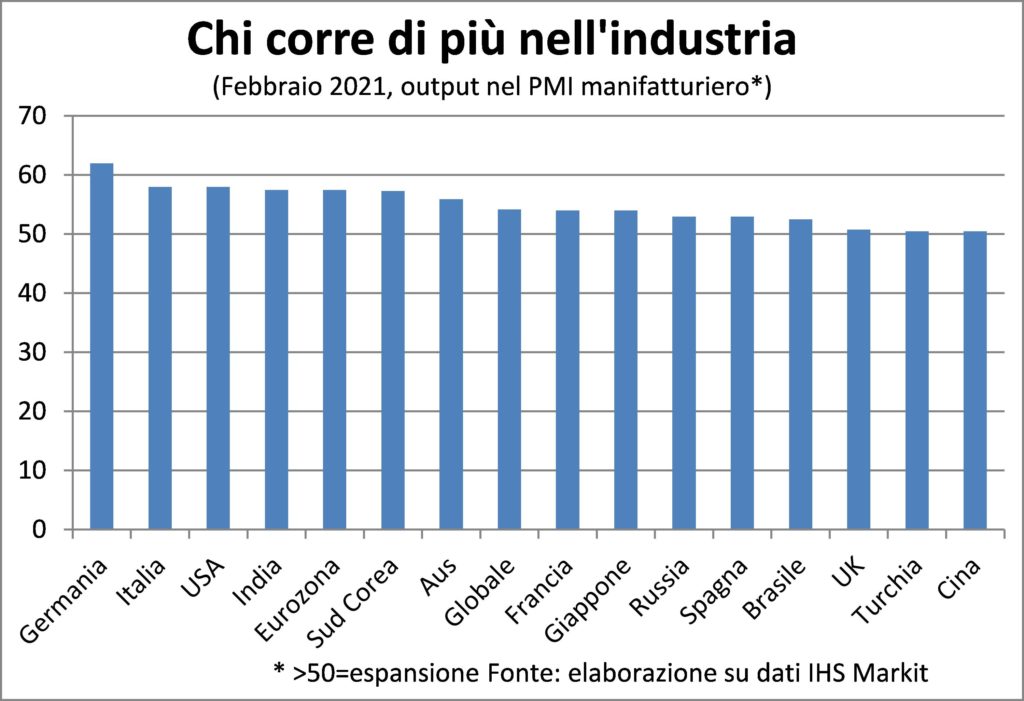

The economy, however, like Orlando, is telling us that the milk of the beast-state is good. He is telling us this through the trend of economic indicators. Industrial production is increasing at a fast pace everywhere. As can be seen from the high level of the output component of the PMI survey. They are in the lead Germany, USA and, hear-hear, Italy.

Among the large industrial countries, only in China fell, apparently signaling deceleration. But it must be remembered that there the manufacturing PMI was just above 50 even when the industry was growing by 15% and counting. Because it is a qualitative indicator that signals how things are going compared to before. And if the Chinese economy now slows down a bit from the pace of the second half of 2020, we would be grateful both because it would still make a large contribution to global growth and because it would ease the pressure on demand and on the already very high prices of raw materials.

The increase in industrial production it is pulled both by household consumption and by investments of businesses. The first ones have reluctantly, chosen to use a little of the many money they find themselves saving in the purchase of material goods, adapted to the domestic life in which they are forced by the restrictions on social life. In the USA, consumption of goods was 10% above pre-pandemic levels in January.

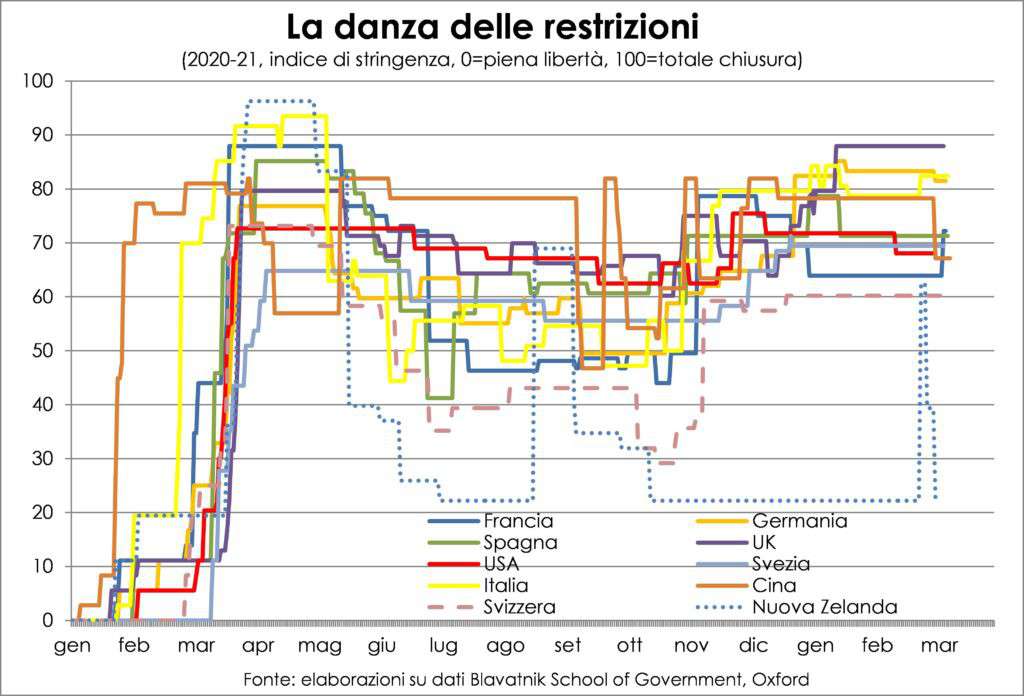

The restrictions will continue, in an exhausting macabre dance of softening and hardening, until the warm season in the northern hemisphere, where 90% of the world's population lives. With the heat, we also saw it in 2020, the virus melts and survives less for long.

Businesses have seen profit margins unchanged, precisely thanks to public intervention, and are spurred to adapt capital to new digital technologies and the transformation of the ways of spending and producing that the pandemic has accelerated.

About those forced savings: Bloomberg has calculated that in the world there is 2.900 billion dollars (2.400 billion euros) of unspent income in excess of what it would have had in normal times, 1,3 times Italy's GDP. About half are in the USA (7,2% of US GDP), one sixth in China (2,7%), and the same number in the four major economies of the euro area (4,9% weighted average). These are savings destined to rise both because there will be more months of life lived with difficulty and because other public aid will arrive.

Vaccines that free from restrictions and spending these savings they will turbocharge demand in the second half of the year. And the ocean liner will turn into a hydrofoil. At least this is the hope and, in the financial markets, the bet. Will this more demand translate into higher prices or higher production?

Dilemma whose answer has consequences of economic and financial policy. But also for the existence of people. If everything or almost everything goes into production, then the extraordinary budgetary and monetary measures can be withdrawn slowly and without haste. If they go in prices, then there is the risk that rates will rise (as they are doing) with strong stock market corrections and the risk of a new recessionary stumbling block.

The anecdotal and statistical impression is that companies don't need to increase margins, on the one hand. And, on the other, they don't play with prices like a yo-yo, because it undermines credibility and trustworthiness. In times of so many and such changes, loss of image can be fatal.

Further, the new and increased demand will go towards sectors that today have a large unused production capacity: catering and tourist services, shows, retail trade, clothing goods, travel (including by car), rental houses. And where there's going to be a lot of competition, to attract that demand. That it will recover little by little because the restrictions will be eased little by little. Because it is not yet known whether future variants of the virus will reduce the immune defense of vaccines. While the current exceptional demand for manufactured consumer goods, which in advanced countries is mostly for replacement, will sag.

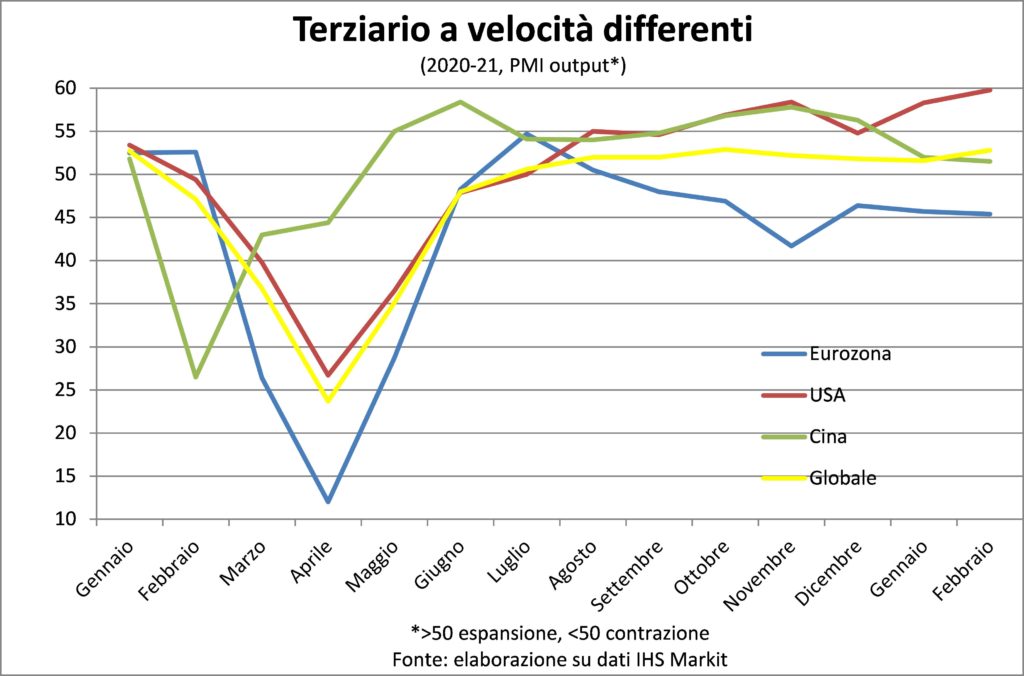

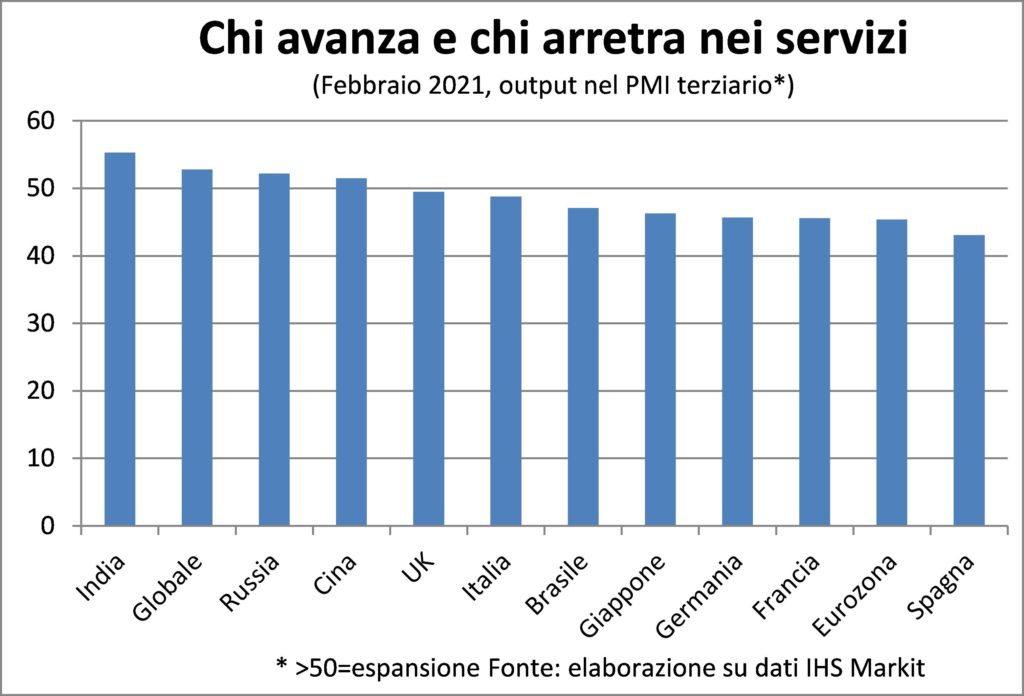

Speaking of the tertiary sector, the relative PMI offers a different and more unequal picture than the manufacturing one. The growth rates are very different. Maximum in the USA and minimum in the Eurozone, with China holding back again. For the latter, the February figure is also marred by seasonal adjustment problems: being the month of the lunar new year, a normal increase in activity is discounted, which however has been kept low in the last two years by restrictions, so that the seasonal coefficients they make it appear lower than it is in comparison with January.

In general, the comments say that the new closures did not affect services the devastating effects of the former. But let's consider that for many sectors the summer recovery had brought activity back to half the pre-pandemic levels. In others even worse. So the fall is from already low values.

Believe in recovery rather than in inflation it is much less demanding than having faith in the Lord (a comparison that does not sound sacrilegious, on the contrary is full of admiration for the not only spiritual commitment of believers). Blaise Pascal invited us to consider this faith as a convenient bet, because at most nothing is lost, but eternal life (in the hereafter) can be won.

In the meantime, let's enjoy the milk of the rhino-state, avoiding picky noses.