The 2014 Mediobanca R&S Yearbook analyzes the large-scale retail sector, including six of the major Italian large-scale retail groups. These are: Auchan-SMA, aggregate of Italian interests which in 2013 represented 10,1% of the group's worldwide turnover (equal to 48,1 billion euros); Carrefour, also Italian interests, equal to 6,4% of the world's 74,9 billion; Gecos, brand Pam (Bastianello family); Italian supermarkets, brand Esselunga (Caprotti family) and of the aggregate of the major consumer cooperatives (nine cooperatives plus two companies controlled by them) operating under the Coop.

The Report also recalls that the activities of Auchan-SMA are headed by the French Mulliez family whose Italian interests reached an estimated turnover of 2013 billion in 7,5 essentially in large-scale distribution, including non-food (Decathlon, Leroy Merlin, Bricocenter and Bricoman). To these five groups are added the Italian interests of the German group Metro, which are equal to approximately 7% of consolidated worldwide (46,3 billion over nine months, of which just under half from cash and carry activities). Since 63% of the Italian revenues of the German group come from electronics and household appliances branded by Media World, the market leader with a share of around 15%, the related data have not been aggregated with those of the remaining operators mostly active in the food segment.

The report shows that in Italy large-scale distribution is characterized by a relatively small presence of large surfaces (>1.000 m53): their share is 80% in our country against 77% in the United Kingdom, 62% in France and 400% in Spain. In fact, the so-called "free service" (surfaces of less than 22 m19) is equal to 400% of the total in Italy, a share that is even higher than the Spanish figure (1.000%). Germany, on the other hand, is characterized by the strong presence of surfaces between 2008 and 2013 m0,3, largely made up of discount stores which represent one of the distinctive features of the German market. The Italian market was particularly penalized by the crisis: large-scale distribution volumes between 3 and XNUMX were stagnant (+XNUMX%) and prices only modestly increased (XNUMX%).

The same parameters referred to European average they marked, respectively, progress equal to 3,5% and 12,7%. This dynamic also depended on the lower concentration of the Italian market where there is a lack of strong leadership by channel and territory: the first three operators represent 34% of the market, against 61% in the United Kingdom and Germany, 54% in Spain and the 53% of France. In 2013, the sales area serving the retail trade settled in Italy at 63,1 million m39, of which 28.232% belonged to large-scale retail trade (food and non-food), the rest to small traditional establishments. The points of sale of the large-scale food distribution stood at 0,9 units, down by 2012% on 17.224.126; the sales area amounted to 0,2 m2012, down by 610% on XNUMX, for an average surface area of XNUMX mXNUMX.

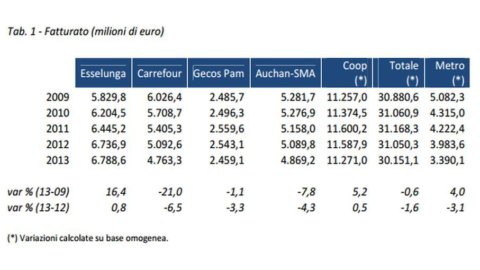

Large-scale Italian non-food distribution counted in 2013 3.665 points of sale, with an average surface area of 2.089 m2013. In 15, the major food retail operators by market share were: Coop Italia (11,4%), Conad (8,4%), Selex (8,2%), Esselunga (7,3%), Auchan (5,9, 4,7%), Carrefour (4,7%), Eurospin (3,6%), Despar (3,2%), Sigma (2009%) and Gecos (2013%). The 2009-2012 turnover of the five Italian large-scale food retail groups, examined here together with Metro, and the relative percentage changes on XNUMX and XNUMX are indicated in the table in the photo.

Sales of the food aggregate fell by 1,6% (on a like-for-like basis) on 2012, settling at 30,2 billion euro. In the last year only Esselunga (+0,8%) and the aggregate of the major cooperatives under the Coop brand (+0,5%) recorded increases. Carrefour dropped by 6,5%, Auchan-SMA by 4,3%, Gecos lost 3,3%. Also examining the four-year period 2009-2013, only Esselunga (+16,4%) and Coop (+5,2%, again on a like-for-like basis) achieved increases in turnover. The downsizing of Carrefour is important, with its turnover falling by 21%. The decline of Auchan-SMA was less marked (-7,8%), while that of Gecos was marginal (-1,1%).

Attachments: GDO Report 2013.pdf