The last -very interesting- working paperr presented by SACE is entitled "East Asia through the crisesi”, by Andrea Pierri, and was created with the aim of analyzing and answering the growing questions about the possible emergence of a new “crisis” for Asian countries similar to the one that struck them in the summer of 1997: today we are faced with what many observers have already renamed “Asia vu"?

To answer this question and outline the future prospects for the Asian region, the causes determining the crisis are retraced in the SACE study, comparing them with the present situation. In this context, the role of China and the regional impacts associated with its slowdown are also explored.

The current phase of the crisis which, which began in the summer of 2007, continues to grip the global economy and whose outcome is not yet known, is characterized by fears of a possible "hard landing” (strong economic contraction) of emerging countries, considered as the second epicenter of the global crisis. Although these economies continue to record significantly higher growth rates than those of industrialized countries, they have slowed down in recent years. Fears of a possible change in the direction of US monetary policy have exacerbated fears about their growth forecasts, causing a general outflow of foreign capital, tightening of financial conditions and currency depreciations.

The liquidity injected by the Federal Reserve (“Fed”) with the expansionary monetary policies of Quantitative Easing (“QE”) it flowed towards those countries for which growth prospects were believed to be greatest: the emerging countries. Suddenly, last spring, there was a fear that the Fed could suddenly withdraw this liquidity from the markets (so-called. Tapering). The markets that had benefited most from it become, as a result of the outflow of capital, the most affected.

Overall, the impact was managed well by most emerging economies, although the effect on some countries was magnified by internal structural problems, such as current account deficits and inflationary pressures. However, concerns remain about what will happen when the QE program is definitively shelved. Today, the biggest fears center on East Asia.

The recurring question, which many analysts are asking today, is whether we may be facing a "déjà vu", i.e. a scenario equal or similar to that which occurred in the summer of 1997.

The SACE study outlines some responses to these hypotheses and concerns.

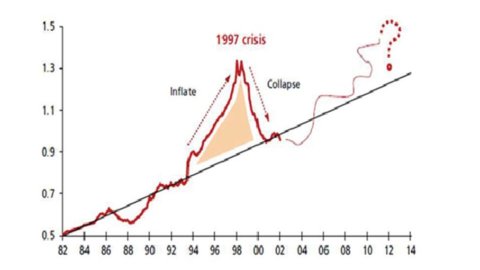

First of all, the similarities and differences between the 97 crisis and the current situation are analysed. The crisis of 1997 arose above all from an excess of credit arriving from abroad, in particular by Japanese and European banks which granted currency loans to local financial companies, which borrowed in dollars and yen (at low interest rates) to buy securities on local markets (at high rates), with the classic phenomenon of the "carry trade". Between 1996 and the first half of 1997, the credit bubble that had given birth to the myth of the "Asian Tigers" began to deflate, losses began to mount, causing a further decline in confidence and further reducing the granting of new loans. Unfortunately, both the decrease in the value of the currency and the increase in interest rates (in an attempt to stop the outflow of capital) caused financial problems for the economy, for finance companies and for businesses. The graphic above gives a glimpse of a dangerous resemblance between that situation and the one that arose after the beginning of the world crisis in 2007: the excessive credit granted to debtors from Thailand, Malaysia, Indonesia, the Philippines, etc. it led to the 97 crisis and produced its serious consequences; now an excess of credit on the area's GDP has also been reproduced in recent years.

However, among the causes of that crisis there was not only the impact of the financial bubble, characterized by excess trust and investment, which occurred in a context of diminishing returns, but also the weak fundamentals of the Asian economies (including excessive currency appreciation, large current account deficits, large short-term external debt and weak domestic financial systems).

In the following years, Asian countries changed the composition of their production: less and less for domestic consumption and more and more for export. Thanks in part to the simultaneous increase in savings, the current account deficit that had characterized the years prior to 1997 reversed abruptly. Since then many countries, in order to create a protection against possible future shocks, have generated substantial surpluses, still today among the highest in the world. The combination of a current account surplus (surplus) and net capital inflows has allowed Asian countries, on the one hand, to accumulate large foreign exchange reserves and, on the other hand, has enabled them to repay their accumulated external debt. Indeed, many Asian countries have turned from debtors to net creditors towards the rest of the world.

However, following the announcement of a possible reversal of US monetary policy, Asia, as well as many other emerging economies, has been subject to a generalized outflow of foreign capital which led to a significant tightening of financial conditions and a depreciation of currencies. In the presence of large capital outflows, central banks, to stem the downward pressure on their local currencies, made extensive use of both market instruments, such as the increase in official rates and operations on the foreign exchange market, and of an administrative nature, such as the easing of restrictions on capital inflows.

This represents an important element of distinction compared to what happened in 1997. In those years, the exchange rates of many countries were fixed and therefore managing the volatility on the financial markets was much more complex than it is today.

The currencies that have currently recorded a more marked deterioration in the exchange rate with the dollar are those of the countries of South and South-East Asia, characterized by negative current accounts, fiscal deficits and sharply worsening economic fundamentals. The two economies most affected by exchange rate volatility were Indian and Indonesian, which have non-marginal internal structural imbalances.

Today, Asian countries are much more “resilient” than they were before the 1997 crisis. They exhibit: (i) high growth rates; (ii) debt denominated in local currency and with a longer term maturity structure; (iii) current accounts with better balances; (iv) flexible exchange rates (making adjustments much easier); and (v) large foreign exchange reserves that can be used to offset capital outflows.

Overall, problems remain, mainly in India and to a lesser extent Indonesia, but recent capital outflows mostly reflect nervousness about a slowdown in QE, rather than structural problems in the region. Fundamentals remain solid and recent fears appear to be overdone. The region as a whole remains far from the excesses that led to the 1997 crisis.

As for China, growth expectations for its economy have gradually been revised downwards over the past two years. Despite having managed to avoid the dreaded hard landing, the Chinese political class seems to have accepted lower and more sustainable growth rates than in the past. According to the latest IMF estimates, GDP should grow by 2013% in 7,6 and by 2014% in 7,3.

For decades, the world's most populous country has relied on a simple formula to boost growth: ample cheap labor and an unprecedented 35 percent to nearly 50 percent increase in investment to GDP. Before. It has invested in infrastructure, especially in roads connecting industrial centers with ports, in the development of telecommunications networks, in the construction of new factories and the purchase of production machinery, all investments which are the basis of a country's development.

The favorable economic context, promoted by the Beijing authorities, and the large investment opportunities have always encouraged FDI entering the country, considered the main tool of knowledge transfer and therefore of development. Now all of these drivers appear to have reached a mature stage: The high supply of cheap labor is running out, employment in factories has reached its maximum capacity, and the highway system is second in the world behind the United States.

The authorities are working on a deep change in the development model that can ensure, in the medium-long term, more sustainable growth than that generated so far by low-cost investments and exports. This will imply lower growth rates than those recorded to date and greater attention to the "quality" of development rather than its "quantity". Lower-rate growth means a less disruptive China, producing less geopolitical friction, and less fear of the rise of the "Red Dragon." So it doesn't necessarily have to be interpreted as negative.

Signs of a dangerous real estate bubble, combined with the slowdown of the Chinese economy and demand will feel their effects on the entire Asian region, especially in the countries of East Asia and Southeast Asia for which China is an important trading partner (primarily Hong Kong, Taiwan, and South Korea.

So what are the future prospects for China? Today, China must face problems that require structural solutions and new challenges that are crucial for its internal growth, as well as for relations with the rest of the world.

At the macroeconomic level, the main changes include: the increase in household disposable income to stimulate domestic consumption, as the main driver of growth and, consequently, reduce the importance of investments and exports.

At the financial level: the liberalization of interest rates and currencies; the globalization of the renminmbi (which in any case is already happening, if it is true that the RMB is already the second currency in world trade, as stated by SWIFT); greater openness to the capital market; the fight against the shadow banking system and the attempt to curb excessive credit growth.

Microeconomic changes include: a reduction in the role played by state-owned enterprises (SOEs); a contraction of savings relative to investment in such a way as to reduce the current account surplus; the introduction of an adequate welfare system; the reduction of air and water pollution; a "healthy urbanization mechanism" that can find a solution to the problem of the lack of services and social protection for all those migrants who today live in the suburbs of major urban centres; greater property rights on peasant lands for a more shared participation in the modernization of the country.

The implementation of these reforms and structural changes will certainly bring with it benefits, but also short- and long-term risks.

The main long-term risk is that these structural changes may prove more difficult than we think.

The short-term risks are even more tangible. The most important is that the growth of domestic consumption fails to fill the gap left by investment and exports, and that the growth of economic activity may slow down more than initially estimated. But in the end, concludes SACE, the greatest risk would be to do nothing.