For days the chancelleries of the main European capitals have been arguing about the opportunity to issue Eurobonds, without realizing that in 2020 alone the ECB promised to buy 1050 billion euros of European bonds, which in fact are equivalent to Eurobonds or even from a macroeconomic point of view are more effective. In fact, they respect a principle of mutuality since they are purchased by a European institution and paid for in European currency. These bonds are then free of charge as the ECB returns to the national central banks of the respective countries all the profits made on these bonds: interest and capital gains. Lastly, the ECB's purchases allow member states to increase the supply of government bonds and reduce their spreads, since they increase the demand for these bonds. This makes it easier for all countries, but especially the most indebted ones, to implement anti-recession policies and increase their public deficits at a much lower cost and without particular pressure on the market.

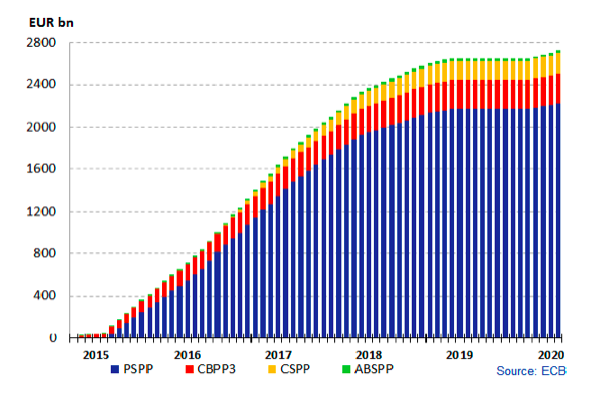

At the end of February, the European Central Bank already had almost 2700 trillion European securities on its balance sheet assets, over 80% public, which have an average duration of seven and a half years. The ECB has also committed to fully reinvest maturing securities “for an extended period of time after the date on which the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favorable liquidity conditions and an ample degree of monetary accommodation”. Thus the effective duration of the securities in the ECB's portfolio is greater than the financial one.

We also recall that the distribution among the jurisdictions of the euro area of the purchases of debt securities will continue to be conducted on the basis of the shares of capital of the ECB held by the individual National Central Banks. However, the ECB statement at the end of March specifies that: "purchases under the PEPP (Pandemic Emergency Purchase Programme) will be conducted in a flexible manner, allowing for fluctuations in the distribution of purchase flows over time"

Thus taking into account that the stake in the capital of the ECB by the Bank of Italy is 13,8%, at the end of 2019 the ECB held almost 370 billion euros of Italian bonds to which another 2020 billion will be added in 145.

Cumulative net purchases of the ECB

While I understand that the battle for the issuance of Eurobonds has a political value very important, because in fact it would make it possible to expand the Community budget and allow for the creation of a safe assets European, the true salvation of Europe will once again come from Frankfurt. To this, in addition to what has already been done, which is unquestionably a lot, we still have to ask for a program of substantial purchases also for 2021, since, even if the health crisis is resolved within the year, it is unlikely that the economic one will not drag on to the next. Furthermore, it would be desirable if the ECB were to undertake to buy back maturing securities for an even longer horizon, say ten or twenty years. In this case, we could actually not worry too much about a significant chunk of our debt and think about economic growth.

Excuse me but I ask due to my ignorance on the subject. So, however, the spread continues to exist. So Italy must borrow at a higher rate than Germany. Instead with Eurobonds the interest rates would be the same for everyone. Seems like a substantial difference to me.